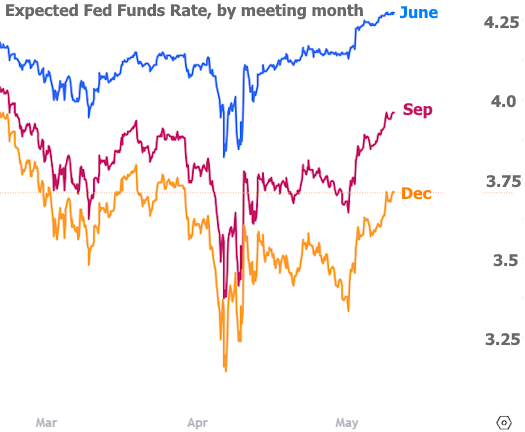

The market is constantly making bets on where the Fed Funds Rate will end up for any given moment many months into the future. As such, that rate expectation is constantly changing. It will continue to change, and it will change in different ways for different time frames.

For example the futures contracts that pertain to June's Fed meeting will indicate a different rate than the contracts for the December meeting. In other words, if traders think the Fed will end up cutting rates, it will be in steps--not all at once.

When Trump's tariff plan was first announced, the market rushed to price in a faster pace of rate cuts, even in the relatively near-term meetings like May and June. After the 90 day pause, rate expectations reversed course, but more so for those near term Fed meetings. Traders still foresaw lower rates when they looked farther into the future.

While there was a Fed meeting this week, it had no impact on these expectations. The Fed was widely expected to say exactly what it said. In a nutshell, evolving trade policies could end up being good or bad for the rate outlook. If there's lots of inflation and economic growth, that would be bad for rates. If there's a lot of economic contraction and less inflation, that would be good for rates. The reality ultimately depends on the details of trade deals and global financial market response.

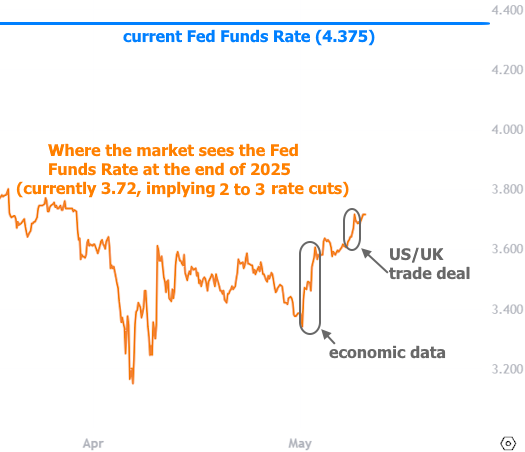

While the Fed couldn't add much to the dialogue this week, end of year rate expectations did finally break above the pre-tariff levels. Most of this move happened at the end of last week owing to stronger economic data. This week's contribution came from the announcement of a US/UK trade deal. The timing is highlighted in the following chart, which singles out only the December Fed Funds Rate expectations. The chart also reminds us that even though expectations moved up, the expected rates are still far below current levels (indicating 2 to 3 cuts of 0.25%).

As always, the Fed Funds Rate is merely on the same family tree as mortgage rates, but the two are quite different at times. Whereas Fed rate expectations are definitely higher now compared to early April, mortgage rates remain a bit lower.

The more one zooms out on a chart of rates, the more the past 2-3 years look like one big, flat waiting game.

Even before tariff changes, we were in the same sideways spot, waiting for a meaningful departure from the uncertainty. Resolution will come from the same places either way: rates will consider the economy, inflation, and the amount of money the government needs to borrow. There are other minor considerations, but these are the big 3, and the finalization of trade deals can have a direct impact on all of them.

The coming week brings the first official, big picture inflation reading for the month of April in the form of the Consumer Price Index (CPI). While it's far too early to fully assess the tariff impact on measured inflation, it's not too early to see some changes. As always, the more that inflation surprises to the upside, the higher the implication for rates, all else equal. The "no surprise" reading for CPI would be a shift from 0.1 to 0.3 in terms of month-over-month core inflation.

Apart from the economic data, there will certainly be updates to digest from the over-the-weekend trade negotiations between the US and China. It's tremendously unlikely that these talks would conclude as quickly as those with the UK, but still very likely that they produce some actionable headlines. In other words, this is another source of potential volatility in rates in addition to economic data like CPI.