Markets began the week with a hangover from last Friday's late-day announcement of a US credit rating downgrade from Moody's with both stocks and bonds losing ground in early trading.

When bonds "lose ground," it means lower prices and higher yields (aka "rates"). While those losses were ultimately almost completely erased by the end of Monday, bonds couldn't find any reasons to keep that momentum going. Conversely, they found several reasons to revisit higher yields, ultimately hitting the weakest levels in several months.

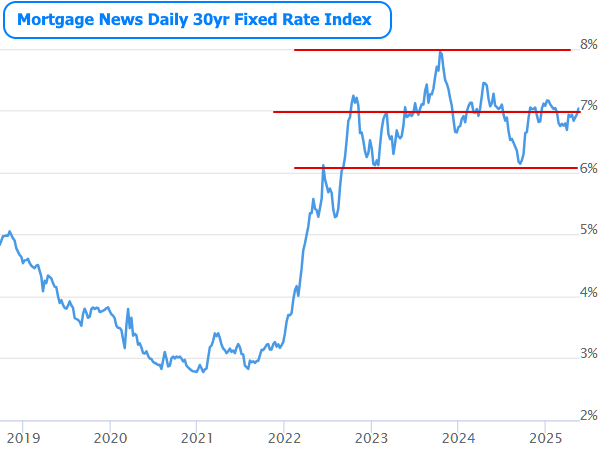

Again, "weakness" in bonds = higher interest rates, and that was on full display in the mortgage market. Mortgage News Daily's 30yr fixed rate index jumped to a 3 month high and remained over 7% for 3 straight days.

7% rates aren't fun, but they're also no new. One need only go back to February to see the better part of a month spent over 7%. In the even bigger picture, the long term high of 8.03% in October 2023 and a subsequent low near 6% about a year later means that 7% is exceedingly "middle of the road."

The problem, for most people, is that it's been the middle of the road for far longer than anticipated. As has been and continues to be the case, there's not much incentive for a big improvement without 1 or more of the following 3 things:

- A sharp and sustained decline in inflation

- A sharp and sustained downturn in economic activity

- A sincere, bipartisan effort to reduce the deficit

Bullet point number 3 was on full display this week as bond traders generally protested an absence of more serious efforts to reduce spending amid congressional debate on the current bill. Why do bonds care? Simply put, the US sells Treasury debt to meet its spending obligations (tax revenue alone isn't enough). Treasuries are like any other economic commodity: the more there are, the lower the price, all other things being equal. And when bond prices fall, rates go up.

The display came to a head on Wednesday afternoon when a 20yr Treasury auction met with somewhat lackluster demand. On any other week, this wouldn't have been a big deal for the market, but with deficit tensions running high, it was seen as the latest endorsement of the bond market's protest.

Bonds improved a bit on Thursday and then again in Friday's early morning hours following Trump's comments on raising EU tariffs to 50%. By the end of the week, bonds were at higher yields than last week, but not quite as high as a few days ago.

A single week is far too narrow a frame of reference for the current challenges. Very little is actually happening in the bigger picture. Rather, the interesting development is what's NOT happening. The month of May is increasingly sending the message that bonds have once again failed to maintain a trend back toward lower yields. This hasn't even been as serious an attempt as the last two (noted by red circles in the chart below). The net effect is a broader trend of sideways to slightly higher yields/rates, and a mortgage market that continues to wait for one of the 3 bullet points above to offer some relief.