The juxtaposition of last week's jobs report and this week's Consumer Price Index (CPI) created a fair amount of volatility, but for fans of low mortgage rates, it's too soon to care.

Whether we're talking about interest rates in general or the Federal Reserve, both are sensitive to any major changes in the economy and inflation. Among economic data, last week's jobs report is the most capable of causing volatility, pound for pound. This week's CPI is the most capable among the several monthly inflation reports.

As we discussed last week, the jobs report was strong enough to push rates instantly (but only moderately) higher. This week's CPI served as a bit of a foil, showing a much lower number than expected. In annual terms, inflation is still not quite back to target levels whether we're looking at the headline number or the core (which excludes food and energy).

But if inflation were to continue at the exact same pace seen over the last 3 months, core CPI (seen as a better indication of underlying trends than the more volatile "headline" CPI) is tracking at below-target levels.

Interest rates are determined by the bond market, so we can watch bonds (like the 10yr Treasury) fluctuate moment by moment to see the implied reaction in rates. Bonds are generally planning on waiting to see if there's any additional inflation in the data after tariff/trade policies are finalized.

That means near term inflation data would be taken with a grain of salt, but this report was enough of a surprise to elicit a response. Taken together with the week's other data, it was enough to briefly fully erase the damage done by last week's jobs report.

The inflation data was so refreshing, in fact, that the market began to entertain an accelerated timeline for the next rate cut from the Fed. Conveniently, there are futures contracts that allow traders to bet on the Fed Funds Rate at various points in the future. Expectations for December 2025 were obviously impacted.

But perspective is important. Not only does the chart above pertain to the December Fed meeting, it is also a fairly narrow range in the bigger picture. If we merely add the September Fed meeting to the chart, we can see how much narrower the range looks. We can also see how much less of a reaction there was in September's expectations.

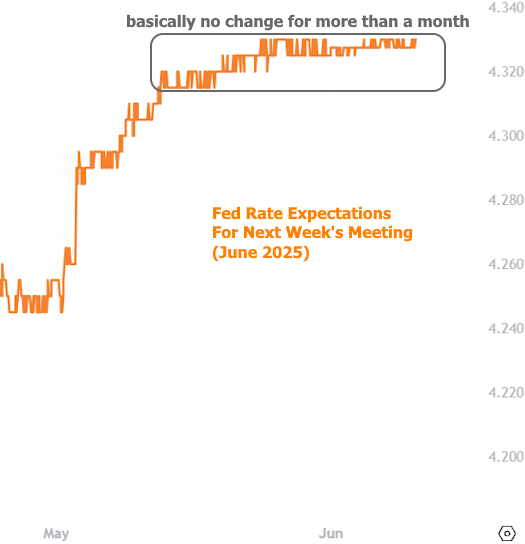

So what happens if we examine the current meeting month? There's not really a point, it's been almost perfectly flat in the "no chance of a rate hike" camp since the beginning of May.

All that to say the Fed is definitely not cutting rates at next week's meeting and the market knows it. The Fed has been very clear in its desire to wait and see if tariffs/trade policy have a measurable impact on inflation AND that it feels justified in waiting as long as the labor market isn't deteriorating too quickly. Last week's jobs report seemed to condone that stance, for now.

Another question that fans of low mortgage rates should consider is whether a Fed rate cut is really the thing they want. History doesn't always repeat itself in exactly the same way, but the following chart is a sobering reminder for anyone who still thinks that Fed rate cuts help mortgage rates:

Any meaningful market volatility from next week's Fed announcement is most likely to result from changes in the Fed's dot plot (a chart in its economic projection materials that shows each Fed member's forecast for the Fed Funds Rate over the next few years).