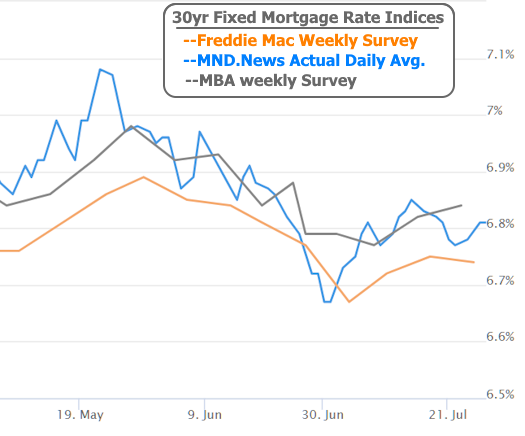

Mortgage rates ended the week at exactly the same levels as last Friday on average. This isn't too surprising given the extremely light and inconsequential nature of this week's scheduled economic data.

Things get highly consequential next week with the arrival of the monthly jobs report—a cornerstone of market movement that nearly always generates one of the biggest trading days of the month. It also carries more rate-moving power than all of this week’s reports combined.

The only report that got a small amount of attention this week was Thursday's Jobless Claims data, which came in stronger than expected and logically pushed rates just a hair higher. But weekly Jobless Claims data isn't remotely in the same league as next week's big jobs report on Friday, nor is there any strong track record of one predicting the other over such short time horizons.

Apart from the claims data, markets continue to digest headlines surrounding Fed Chair Powell and whether the administration might try to force an early departure. For now, that concern has cooled thanks to clarifying comments from Treasury Secretary Bessent earlier in the week and from Trump himself later in the week.

The most recent issues surround the notion that the Fed has spent too much money on a massive renovation/retrofit of its D.C. offices. But after touring the construction site this week, Trump said of the cost overruns, "it happens," it shouldn't be grounds to remove Powell, and there is no pressure for him to resign. The bond market improved slightly in response, but not enough to impact mortgage rates.

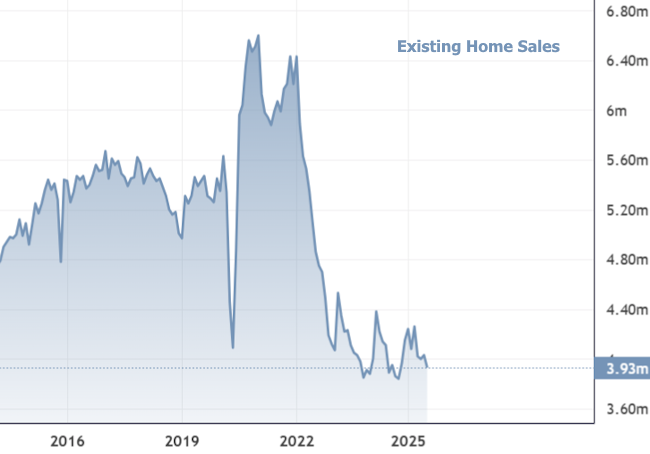

As for housing, not much has changed. Recent data showed that both new and existing home sales remain stuck in a rut, with affordability and inventory challenges keeping activity subdued.

The silver lining is that homebuilders continue to adjust—cutting prices and expanding inventory—while home prices overall remain historically high. Ultimately, rates remain range-bound for now.

That could change quickly depending on how next week’s jobs report shakes out. Prior to the jobs report, there are many other noteworthy events on the calendar. Some of these are economic reports with the most notable being Tuesday's Job Openings, Wednesday's GDP (first glimpse at Q2), and Thursday's PCE inflation. Some are non-economic events such as the Treasury auction cycle on Mon/Tue and the Fed rate announcement on Wed.

This raises an important question, but one that's easy to answer: will the Fed cut rates next week? Not a chance. So why is it important?

By the time a Fed meeting finally rolls around (only 8 times a year), the market has largely already determined whether or not there will be a cut or a hike. That leaves the focus on any verbiage changes in the Fed announcement text or any shift in tone from the Fed Chair at the press conference that always follows the official announcement. Given that the Fed is getting closer to considering cutting rates, we could indeed see such a tone shift. But no matter what transpires on Fed day or with the ancillary calendar events, all bets are off until we see Friday's jobs report and the resulting move in rates.