Last Friday's jobs report sparked a big rally in the bond market, and thus a big improvement for mortgage rates. This week was very light in terms of market data and volatility, but it helped solidify the improvement from the jobs report.

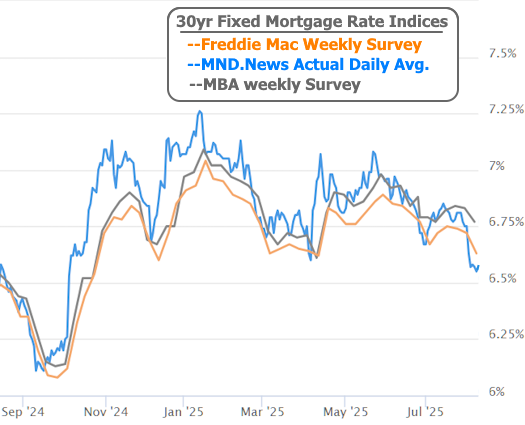

Specifically, the average lender wasn't even able to fully adjust their rates to account for market movement last Friday. When bonds maintained those gains through Monday, it was safer for lenders to adjust their offerings to reflect the bond market reality. With that, the week began with rates at their lowest levels since October 2024. Things remained very calm and sideways after that.

There were a few moments where the market could have gone off-script, most notably with Tuesday’s ISM data--a key report on the health of the services sector. While the report’s inflation component hit another post-pandemic high (bad for rates), the rest of the numbers painted a softer economic picture. Traders ultimately gave more weight to the slowdown signals, helping bonds and mortgage rates hold their ground.

Other economic reports, like jobless claims, came and went without much impact. Even a poorly received 30-year Treasury auction (which should have been bad for rates) failed to deter bond traders, thus keeping rates in the same lower range. In short, the market remained remarkably resilient with only tiny day-to-day changes.

Next week could be a very different story. Tuesday’s Consumer Price Index (CPI) will provide a critical update on inflation and may shed more light on how recent tariff changes are impacting prices. Several Federal Reserve officials are also scheduled to speak, offering an opportunity to gauge whether last week’s weaker jobs data has shifted their willingness to cut rates. Between these two factors, the calm we’ve seen this week could give way to a much more volatile landscape in the days ahead.

As always, volatility can play out for better or worse. September 2024 proved that rates are capable of hitting the low 6's under the right circumstances while early 2025 suggests a ceiling just over 7%. Low 6's would require several lower inflation reports and more downbeat employment data. Conversely, we wouldn't immediately shoot back over 7% after 1 bad week of data. But if CPI is sharply higher or lower than expected, rates will definitely take a step in one direction or the other.