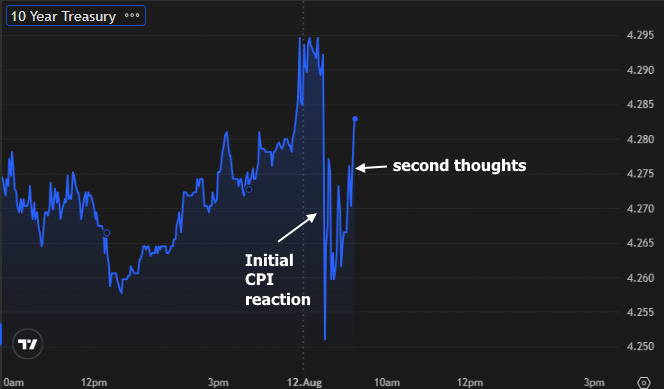

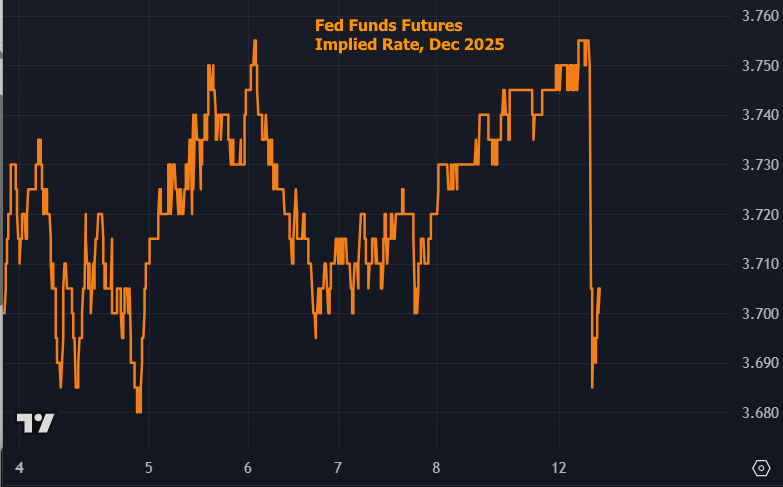

There's something for everyone in this morning's CPI data. The monthly headline was on target at 0.2 vs 0.2. Same story for the core at 0.3 vs 0.3. Bonds are just a hair stronger, but it's hard to make a case that they should be based on other internals:

- The unrounded monthly core was 0.322 versus the median big bank forecast at 0.31

- Supercore (core CPI excluding housing) was 0.481 vs 0.212 previously

- Core goods (tariff sensitive) is now 1.2% year over year - highest since June 2023

All these bullet points argue for bonds to be selling off today and likely justify the backpedaling in the initial rally. Bonds are still modestly green on the day, but right in line with yesterday's range. It wouldn't be a surprise to see gains continue to erode as markets digest the implications.