If you read nothing else below, read this: people are talking about stronger odds of a Fed rate cut in September. Some people assume this means mortgage rates would move lower after that potential rate cut. Those people are wrong, and there is memorable evidence from late 2024 when mortgage rates moved quickly higher from long term lows mere days after the Fed's September rate cut.

September 2025 may or may not follow the same pattern. We won't know until we see the economic data in October and beyond. After all, it was the data in those months that pushed rates higher last year. The long-term lows for mortgage rates came courtesy of weaker econ data in the summer months which fueled expectations for the September cut. Mortgage rates move with those expectations more than anything. By the time the Fed actually holds its scheduled rate-setting meeting, the rate market has already moved on to react to new data.

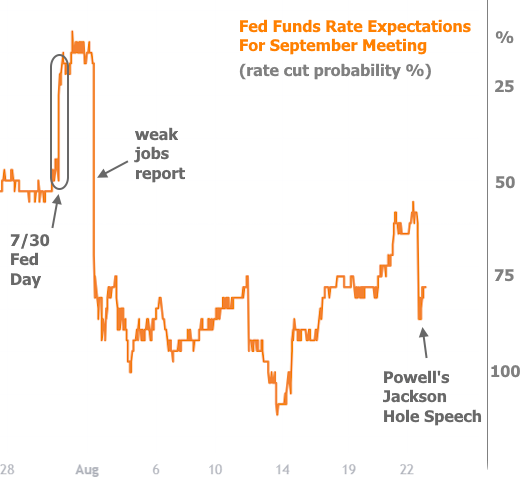

This dynamic is relevant once again because the market foresees a better-than 80% chance of a September rate cut. Those odds improved noticeably on Friday after Fed Chair Powell's speech at the Fed's annual Jackson Hole Symposium.

Powell's speech was the only event on this week's calendar that held much promise for motivating any major movement in mortgage rates. Not only did it deliver on that "promise, but it did so in everyone's favorite direction.

Powell didn't necessarily say anything too surprising. He still sees conflict between the Fed's dual goals of promoting a healthy job market and keeping inflation in check. Friday's speech reiterated that fact, but it did more to acknowledge incremental weakness in the job market.

Previously, strong jobs numbers meant the Fed could afford to keep rates steady at higher levels while they waited to verify that tariffs wouldn't cause more inflation than expected (higher inflation suggests a higher Fed Funds rate, all else equal).

The last time we heard from Powell on this balancing act, it was at the press conference following the July 30th Fed announcement. Two days later, the big jobs report came out much weaker than expected. In addition, the previous two jobs reports were revised sharply weaker, thus completely changing the generally stable vibes in the labor market data. Financial markets have been waiting to see if that would cause a shift in Powell's willingness to consider rate cuts ever since.

To be fair to the market, traders began betting on September rate cuts with much higher probabilities on the day of the jobs report, but traders tend to avoid fully committing to these sorts of shifts until getting clearer confirmation from the Fed Chair.

Friday's speech offered enough of that confirmation for markets to increase bets on a September cut. It's these expectations that drive day to day movement in the rest of the rate market (by the time the Fed actually cuts, the market has long since priced-in that likelihood).

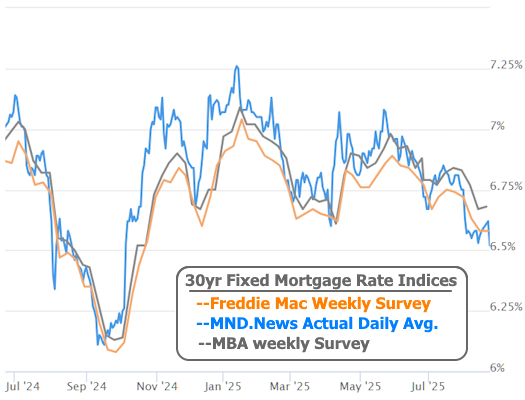

With that, mortgage rates saw their biggest drop since the August 1st jobs report, just barely beating out August 13th's lows to claim 2025's lowest spot. October 3rd, 2024 was the last time the average 30yr fixed rate was any lower.