The underlying bond market (which dictates the rates offered by mortgage lenders) weakened moderately overnight. Weaker bonds equate to higher rates, all else equal.

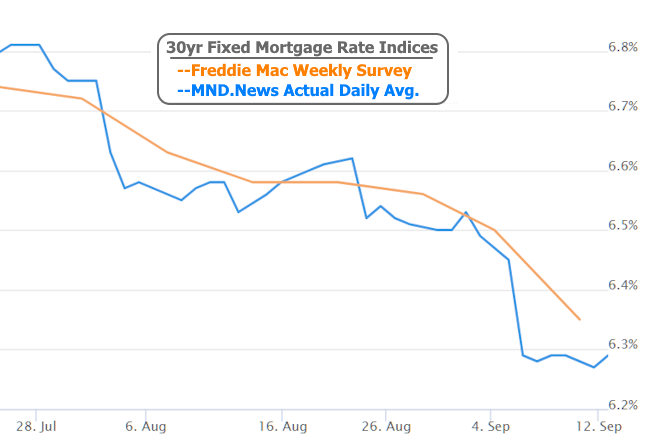

"Higher rates" is contrary to many media outlets' coverage this week, but there's an important reason. Most news organizations that cover mortgage rates rely on Freddie Mac's weekly rate survey for their once-a-week update. Additionally, when Freddie's rate raises/falls appreciably, it receives even more attention.

This frequently creates problems due to the timing and methodology of Freddie's survey. Specifically, the survey is an AVERAGE of the rates seen over the 5 days (Thu-Wed) leading up to Freddie's Thursday release. As such, if rates happen to fall sharply on a Friday (as was the case last week), our DAILY rate tracking will reflect that on Friday while Freddie won't catch up until the following Thursday (yesterday, in this case). By that time, rates hadn't moved any lower, and now today, they're actually a bit higher.

All that to say, the rate drop you're hearing about from Freddie is the same rate drop we told you about last Friday. There's been no meaningful improvement since then, and in fact, a modest increase in rates today.

Today's move in bonds/rates wasn't driven by anything specific and shifts of this size don't demand concrete justification in underlying data or events. It could simply be the case that traders were closing out trading positions for the week and the modest uptick in yields/rates was the incidental result.

Mortgage-specific bonds were even less volatile today, resulting in a mere 0.02% increase in the average 30yr fixed mortgage rate. That brings our index back up to 6.29%, which is in line with this week's other highs and still part of a very narrow range that represents the lowest general levels since October 2024.

Next week brings a much-anticipated Fed announcement. The Fed is virtually 100% likely to cut the Fed Funds Rate by 0.25%. This near-certainty is already baked into today's mortgage rates and the Fed rate cut will have zero impact on mortgage rates in and of itself. Rather, other data release in conjunction with the rate cut could still cause volatility.

The Fed's "dot plot" (a summary of each Fed member's view of the appropriate Fed Funds Rate at various future dates) is of primary importance. The dots help markets gauge the potential path of additional rate cuts in 2025 and beyond. It is a vital tool in calibrating the evolution of the Fed's rate-friendliness as a function of recent economic data. In simpler terms, it will show us how much more willing the Fed is to cut rates in light of recently downbeat labor market data and still-elevated inflation.