Every now and then, a Thursday comes along where we have to set the record straight on what is actually going on with mortgage rates. That's because Freddie Mac releases its weekly mortgage rate survey on Thursdays and its methodology can cause confusion in the mortgage market.

This particular Thursday is an especially treacherous minefield of misinformation due to the juxtaposition with yesterday's Fed rate cut. There are already too many people out there repeating the faulty notion that the Fed rate cut means lower mortgage rates. Adding fuel to that fire are various headlines today (quoting Freddie's data) saying that mortgage rates have fallen to the lowest levels in more than a year.

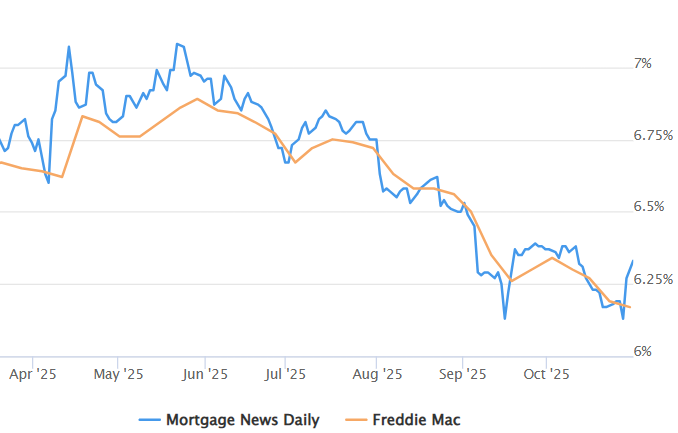

Mortgages rates certainly WERE at the lowest levels in more than year when we reported that fact on Tuesday. But what a difference 2 days make...

Actual daily average rates are up 0.20% since then--the fastest 2 day rise since the exact same thing happened after last month's Fed rate cut. We'd urge those who didn't absorb the lesson back then to do so today. Bottom line: mortgage rates had already responded to all of the news and data that resulted in the Fed rate cuts. By the time those cuts actually happen, they have no additional power to influence rates (other than the Fed Funds Rate itself, which is not a mortgage rate except in limited cases specific to Home Equity Lines of Credit based on the Prime Rate).

How does Freddie get it so wrong? They don't. They just get it "so late." Freddie is reporting their rate as an average of last Thursday through this past Wednesday, and 4 out of those 5 days saw exceptionally low rates. As we noted yesterday, mortgage rates were already surging higher, but not until the afternoon. This means even yesterday's rate spike was too late in the day to push Freddie's average any higher. In other words, it was perfectly bad timing for Freddie's Thursday release to be as low as it possibly could have been.