Not all rates are created equal and not all rates move in the same direction for the same reasons. One of the most common reasons for rates moving in opposite directions is that the underlying bonds, loans, etc. have different terms. In other words, market demand for a 7-year loan can be quite different from a 1-day loan, depending on the day.

While a typical mortgage may be ABLE to last 30 years, most last about 7. Contrast that to loans based on the Fed Funds Rate, which last no more than a day in a majority of cases. This is one reason that mortgage rates often correlate poorly with the Fed's rate, even over intermediate time frames.

But if we want to dig into the most paradigm-shifting breakdowns, we can forget all that boring stuff about loan durations and simply consider timing. In fact, let's say that mortgage rates correlate perfectly with the Fed Funds Rate. We only need to throw the timing wrench into the mix to cause the correlation breakdown.

Specifically, mortgage rates can change every day (sometimes a few times per day) while the Fed Funds Rate can only change 8 times a year under normal circumstances. That gives mortgage rates 6 full weeks to make fine-tuning adjustments that the Fed Funds Rate must make as a single adjustment on a single day.

In addition to timing constraints, consider that we're dealing with financial markets here. Investors will always do everything in their power to adjust trading levels to reflect everything that can be reasonably known about the future. As such, if the market is virtually certain that the Fed will be cutting rates at any upcoming meeting, those expectations are already baked into any rates that have the ability to move more nimbly (like mortgage rates).

Simply put, the Fed rate cut was long since priced in to any consumer rates that share any remote correlation.

But all of the above only explains why mortgage rates didn't move lower after Wednesday's Fed rate cut. We'll also need to explain why mortgage rates moved sharply higher on Wed/Thu.

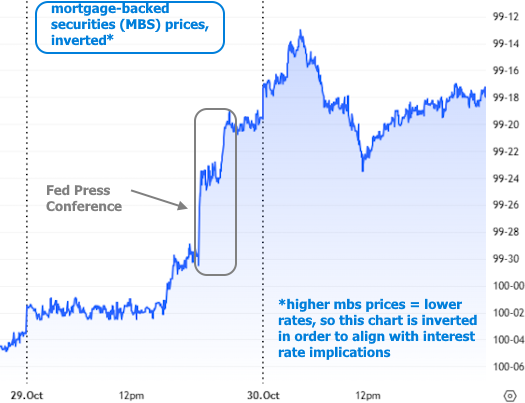

Mortgage rates move on any given day in response to new information. The Fed rate cut was old information, but the comments during Powell's press conference were new. The tone was somewhat unexpected. Whereas the market had been almost certain that the Fed would be cutting rates again in December, Powell was clear to say that this is not a foregone conclusion ("far from it," in his words).

This gave us an opportunity to see how mortgage rates actually correlate with the Fed Funds Rate: via expectations. Powell's comments led to a sharp shift in expectations for a December rate cut. The bonds that underlie the mortgage market made a similar shift in a similarly timely fashion. The result: immediately higher mortgage rates on Wednesday afternoon with additional follow-through on Thursday morning.

The following chart shows that impact in terms of the actual bonds that dictate mortgage rates: MBS (mortgage-backed securities). The chart is inverted such that the line moves in the same direction as interest rates.

NOTE: The idea of higher rates this week runs counter to some national headlines due to Freddie Mac's weekly mortgage rate survey. As a reminder, Freddie's survey is an average of Thursday through Wednesday, reported each Thursday morning. That means Freddie's rate didn't reflect any of this week's rate spike drama. In fact, it was perfectly timed to avoid it. This is also why we can already be virtually assured that Freddie's rate will bounce back up next week as it gets caught up with the day-to-day reality.

In the bigger picture, this week's rate spike isn't too dramatic, but it does reinforce the notion that larger victories for rates will depend on a deterioration in economic data. Measuring such a deterioration is currently a challenge without the full gamut of economic data from the US government (due to the shutdown). The implication is that rates could have a tough time challenging this week's lows until the shutdown ends and the data is flowing.