After the longest shutdown in history the U.S. government reopened on Thursday. As expected, this has added a bit of upward pressure for rates. Because the prevailing rate range is very narrow, this leaves average 30yr fixed rates in line with their highest levels in more than 2 months.

Why would the reopening push rates higher?

Rates tend to move higher when the economy is doing well and lower when economic data is softening. A prolonged shutdown was expected to hurt economic growth. The reopening is thus a net-positive for the economy (compared to an even longer shutdown) and a net-negative for rates.

What else is contributing to higher rates?

This week saw an uncommonly unified message among multiple Federal Reserve officials. Rates are always digesting available comments from Fed speeches and events. There's usually a healthy balance of comments that are friendly vs unfriendly for rates. This week's comments were uncharacteristically unfriendly.

In what way were Fed comments unfriendly?

The Fed generally tries to balance the impact of its policies between two factors: a strong jobs market and stable inflation. Up until this week, they had been expressing more concern over the jobs market and that meant stronger odds of a December rate cut. This week's shift saw multiple Fed speakers downplay recent job market concerns and instead focus on the fact that inflation is still too high. Here are several examples:

Cleveland Fed Pres Hammack: Monetary policy is currently barely restrictive, if at all. The Fed must reduce inflation to maintain credibility. I expect above-target inflation for two to three more years

Kansas City Fed Pres Schmid: Inflation is too hot. Labor market is cooling, but largely in balance. Further rate cuts won't patch job market cracks and could do damage to inflation.

Atlanta Fed Pres Bostic: Fed Funds Rate should stay steady until we see clear evidence of inflation moving toward 2% target

San Francisco Fed Pres Daly: It's premature to say cut or no cut in December

Minneapolis Fed Pres Kashkari: Inflation still too high at 3%. I see mixed signals from the economy. Did not support October cut, and has no strong inclination yet on December rate cut

St. Louis Fed Pres Musalem: previously supported rate cuts to protect labor market but now sees need to proceed with caution on additional cuts

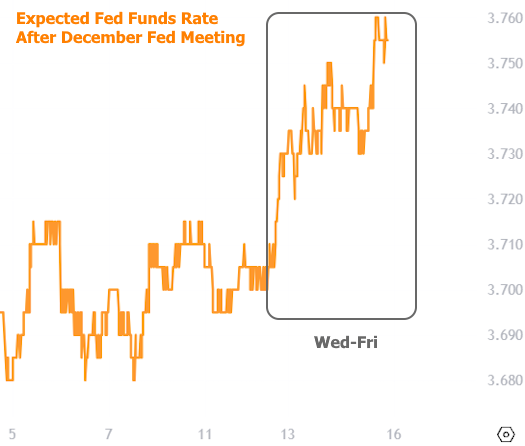

Again, this is a noticeable shift from the average Fed comment leading up to the late October Fed meeting. The market concurs, as seen in expectations for a December rate cut. The following chart shows the implied level of the Fed Funds Rate after the upcoming December meeting based on Fed Funds Futures (the securities that allow traders to bet on the level of the Fed Funds Rate).

Longer term rates had a more varied performance, but also moved decidedly higher on Wednesday through Friday. This can be seen in the following chart of 10yr Treasury yields (for those curious, Friday's temporary dip coincided with sharp losses in stocks. When stocks rebounded, so did bond yields).

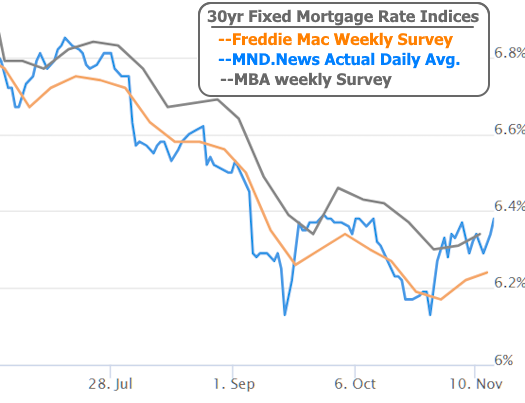

The net impact on mortgage rates was a move back to the high boundary of the 2-month range.

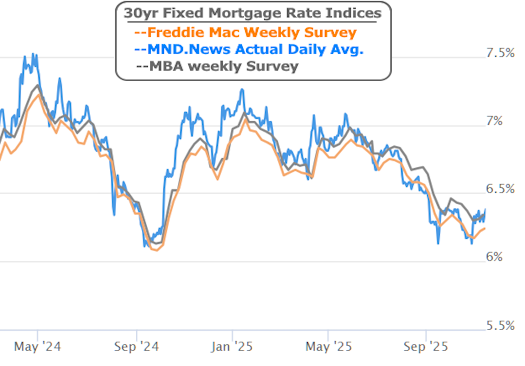

While that sounds like fairly bad news, the range is still low and narrow in the bigger picture. Here's a longer-term view of the same chart:

Looking ahead, markets will be eager to see what the reopening of the government means for the various economic reports that had been on hold due to the shutdown. It's not as if much of the data is ready to go and can simply be released on time. We only had a few updates by Friday afternoon and they pertained to data that would have been released more than a month ago. In the coming week, we expect to get a revised schedule of economic releases. Hopefully, it will include big-ticket reports that come out before the mid-December Fed meeting.

Note on 50yr Mortgage News

Headlines circulated this week regarding the potential for a 50yr mortgage option from Fannie/Freddie. It's important to know that nothing has been officially announced or decided. It may well never come to pass. Even if it does, a 50yr mortgage would have higher rates than a 30yr mortgage, thus mitigating most of the payment savings not to mention vastly increasing interest expense over the life of the loan. There's no way to know exactly how much higher rates would be--only that they would be higher. Best bet: wait to draw any conclusions until we know if it's actually happening. Even then, it will be hard to assess the implications until we see how the market determines 50yr rates.