This week marked the return of delayed economic data from the government shutdown. Specifically, we received the important jobs report that was set to come out in early October. While this is September's data, and thus a bit stale, it was nonetheless responsible for the biggest volume spike in the bond market since the last Fed meeting. Such is the power of the jobs report relative to other economic reports.

Big volume frequently accompanies big movement in bonds/rates, but in this case, there wasn't too much movement. The stalemate was a product of mixed messages inside the jobs data. On one hand, the count of job creation in September easily exceeded expectations (119k new jobs versus a median forecast of 50k). On the other hand, the previous month's payroll creation was revised down to -4k from +22k.

There were mixed messages on the other side of the report which consists of a survey of households that inquires about employment status. The so-called "household survey" is responsible for generating the official unemployment rate. In September's case, unemployment ticked up to 4.4% from a previous reading of 4.3% (also the median forecast for this week's report).

This is the highest unemployment reading for this cycle. In and of itself, this would suggest a decent drop in rates, but there were caveats here as well. Specifically, the labor force participation rate also increased by 0.1%. This means more people in the household survey considered themselves to be in the jobs market. Assuming an unchanged amount of jobs available, an increase in the participation rate would create an equal increase in the unemployment rate. In other words, the 0.1% increase in the unemployment rate isn't as downbeat because it occurred in concert with an increase in labor force participation.

To be clear, participation is more of an ancillary consideration. The unemployment rate is still more important and that's why rates ultimately had a positive reaction to the jobs report--just not quite as positive as it might have been absent the uptick in the participation rate.

Throughout the week, there was a general correlation between heavy losses in stocks and modest improvement in bonds/rates. This correlation is never a guarantee, but it's slightly more likely at times when stocks are making bigger moves. It also helps explain the uptick in Treasury yields after they bottomed out on Friday morning.

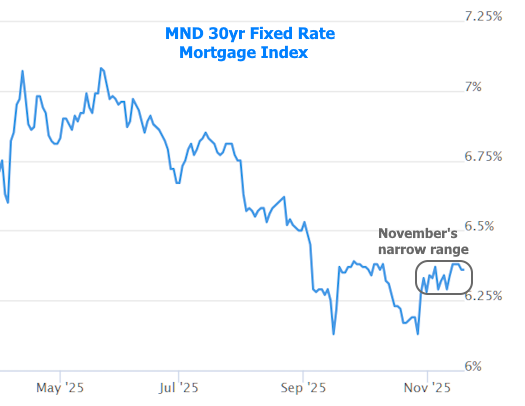

A longer term chart helps put the correlation in perspective. The past several weeks have marked a fairly large correction in stocks. Meanwhile, bonds have been holding a narrow, sideways range.

Nine times out of ten, if Treasury yields are holding a narrow, sideways range, the same can be said for mortgage rates, and the past several weeks are no exception.

Looking ahead, rates will require more econ data in order to make up their mind on the next big move. This is a challenge because other reports delayed by the shutdown will take more time than normal. Data agencies have released updated schedules for most reports and unfortunately, the most important ones won't arrive before the December Fed meeting. That means December 10th will be the first Fed announcement in a long time that truly has potential to go either way in terms of a rate cut. This also increases the potential rate volatility associated with Fed day.