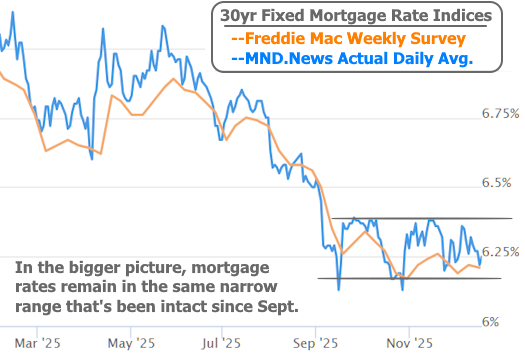

The two most important economic reports of the month were released this week. Both showed promising results for rates, and although rates improved, the reaction was smaller than expected.

First up was November's jobs report, which came out on Tuesday morning. It showed the highest unemployment rate since 2021 at 4.6%--well above the 4.4% forecast.

Under normal circumstances, this would have resulted in a fairly sharp drop in rates. But in the current case, the underlying bond market barely budged.

There are a few specific reasons this may have been the case:

- The participation rate also increased by 0.1%. This means more people consider themselves part of the labor force. When this metric moves higher, it limits the negative implications of higher unemployment to some extent.

- The unrounded unemployment rate was 4.564% vs 4.440% in September, just barely more than a 0.1% increase.

- A substantial majority of the increase was attributable to workers on temporary layoff.

Taken together, these factors go a long way toward counteracting an otherwise gloomy message for the labor market (and a friendly message for interest rates).

The next big-ticket report was November's Consumer Price Index (CPI) which came out on Thursday. We already knew the data collection for this report was impacted by the government shutdown, but inflation came in so far below economists' forecasts that traders were hesitant to trade accordingly. To be fair, bond yields and mortgage rates did hit their best levels of the week shortly thereafter, but most of that movement was already in place before CPI came out.

A final consideration in the rate market's underwhelming reaction is the fact that it's the 2nd half of December and there's always a caveat for inconsistent trading this time of year. Combine that with doubts about the data collection, and traders are content to wait for the next set of reports in January before getting back in a more normal rhythm.

The next two weeks will be even more deeply affected by holiday trading vibes. Markets are closed on Christmas Day and bonds will close early on Christmas Eve. While Friday is technically a fully open day, it will have drastically lower participation than normal. The same pattern of closures repeats the following week (Wed = half day, Thu = closed, Fri = might as well be closed). The implication is that rate movement can be more random and subject to change until new econ data starts coming out in January.