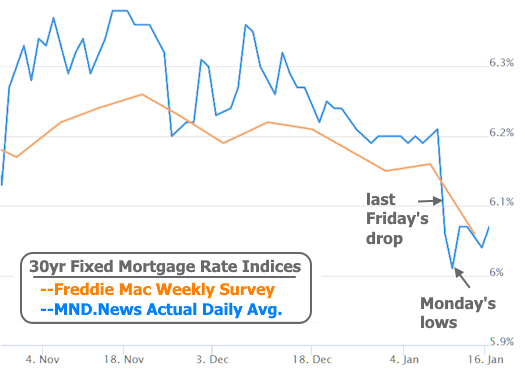

First things first: if we take the last 5 days out of the equation, today's mortgage rates are still the lowest since early 2023. But they spent most of those last 5 days moving up from even lower levels.

The changes are small in the big picture, but the distinction is important considering widespread reporting based on Freddie Mac's weekly rate survey. Freddie's data comes out on Thursdays and thus didn't have a chance to account for the big drop in rates seen last Friday. Similarly, the data wasn't able to account for the upward movement in daily rates seen throughout the present week.

Last week's big drop came courtesy of an announcement that Fannie and Freddie (collectively, "the GSEs") would be purchasing $200 bln of mortgage-backed securities (MBS)--the bonds that directly dictate mortgage rates.

GSE MBS purchases can't single-handedly change momentum in the broader bond market, but they can cause mortgage rates to fare much better than their classic benchmark, the 10yr Treasury yield. That's a good thing right now considering the 10yr yield just broke up and out of its recently narrow range.

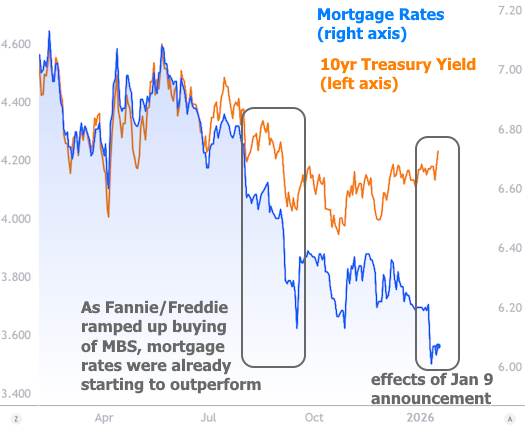

GSE MBS purchases have made for a stark contrast between mortgage rates and Treasury yields. The left side of the following chart is a more normal correlation, but it began to break down several months ago. We now know that Fannie and Freddie were already net buyers of MBS at the time and this certainly accounts for at least some of the divergence between these two lines. Last Friday's official announcement left nothing to the imagination.

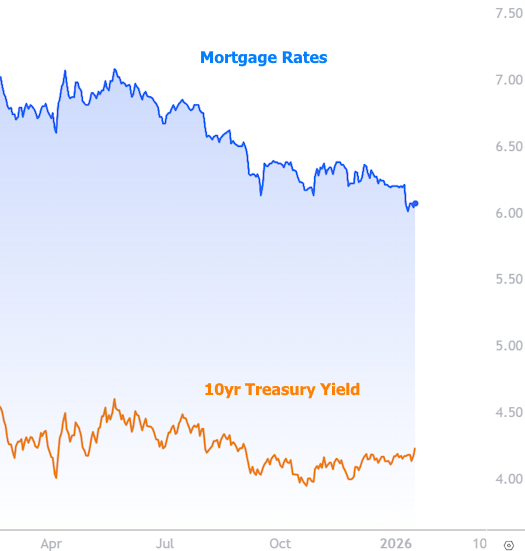

Keep in mind, in the chart above, each line has its own axis in order to highlight the relative performance. If both shared a single axis, the chart would look like this:

Long story short, broader bond market momentum has been placing upward pressure on rates overall, but GSE MBS purchases have more than offset that negative momentum when it comes to mortgage rates. Looked at another way, if Treasury yields were trending lower over the past few weeks, mortgage rates would likely be well under 6% for a top-tier 30yr fixed at the average lender.

With that in mind, what are the prospects for friendlier momentum in Treasuries? That topic remains open to debate. While they may have broken above their most recent range, this is a drop in a much larger bucket. In the bigger picture, bonds continue consolidating in a much wider range as they wait for better justification for a true breakout.

What factors will be considered in determining momentum? Bonds care about several things. One of the biggest is Treasury issuance and that's not something that changes quickly. Given the present deficit/spending levels, issuance will prevent rates from moving down anywhere close to the record lows seen in 2020-2022. But if other factors align, there could still be meaningful improvement.

Those other factors are largely in the realm of economic data with a specific focus on inflation and the labor market. This week's inflation data did no harm, but inflation hasn't fallen quickly enough to constitute a tailwind for rates.

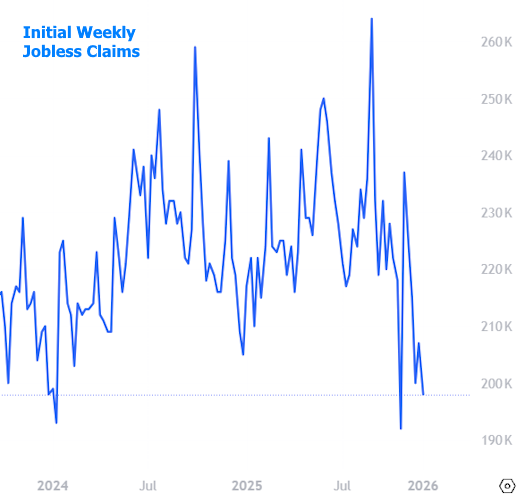

Labor market resilience has been an even bigger counterpoint. The market is definitely paying attention based on Thursday's reaction to weekly jobless claims numbers (a report that doesn't reliably have an impact on bonds). But this time around, the data was much stronger than expected (strong jobs data = bad for rates).