While the word "regime" is often seen in a geopolitical context, it's also common in financial markets. With respect to rates, the most recent regime involved steady improvement starting in May 2025 and ending 3 weeks ago. Since then, a new regime has been taking over and it kicked into high gear this week.

Under the previous regime, bonds (which dictate rates) were operating on the following principles:

- generally stable economic data, but with some uncertainty about the strength of the labor market

- gradually cooling inflation that was likely to continue

- central banks (like the Fed) that were expected to cut rates by September and then hold steady before cutting rates again when data allowed

- foreign central banks that were also more likely to cut rates

- Treasury issuance (bad for rates) that was at least flat and had some hope of remaining that way

Under the new regime, which began with the Iran war but kicked into higher gear over the past 3 days, bonds are thinking about:

- inflation that was still too high for the Fed to cut rates, even before recent events

- an oil/energy/material price spike that further exacerbates global inflation expectations

- the same old uncertainty about the labor market, but not enough of it to really help rates

- central banks that are no longer expected to cut rates any time soon, but who instead may consider rate HIKES

- Treasury issuance that is likely to increase due to war funding and tariff refunds

There's no question that oil prices had been a dominant focus for the bond market for the entire month. The following chart shows oil futures and 10yr Treasury yields (a common benchmark for longer-term rates like mortgages). Starting Wednesday afternoon, we can see yields move higher, even as oil stays fairly flat in the bigger picture.

One very simple reason that bonds and oil behave differently over these shorter time horizons is that the bond market move is nowhere near as significant as the oil move in an even bigger picture.

Rates also had their own reason to move higher due to shifts in tone from central banks.

The Fed kicked things off on Wednesday when Powell said the Fed would need to see improvement in "core goods" and "non-housing services" inflation before considering another rate cut, and that this was true even before considering impacts from rising oil prices. Powell referred to the progress on those two fronts as "disappointing" and while he said rate hikes were not a base case, he didn't rule out the possibility.

Markets didn't love that, but they might have been able to cope with it a bit better if the Bank of England (BOE) and the European Central Bank (ECB) didn't send similar messages the following day. By Friday morning, European bond markets were in panic mode with British yields surging to the highest levels since 2008 and EU yields at the highest levels since 2011. It's hard to overstate how problematic the European influence has been, but easy to understand the concern in those markets (which are infinitely more dependent on imported petroleum products than the U.S.).

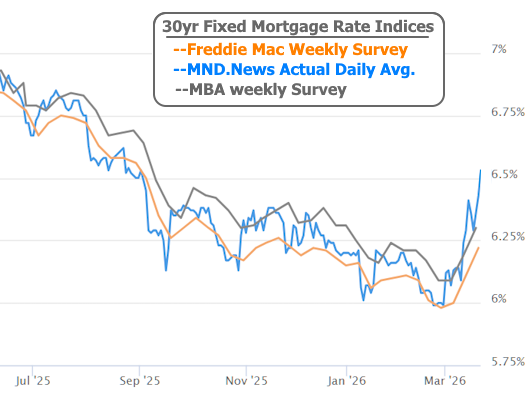

Any time the broader bond market is doing what it's doing, mortgage rates probably aren't having a good time, and this week is no exception. After hitting 5.99% as recently as 3 weeks ago, daily top-tier rate indexes are back over 6.5%--highest since September 3rd, 2025.

When these sorts of regime shifts are happening in the bond market, they don't tend to reverse course quickly even though we can see individual days (or even weeks) that make it seem like the tide has turned. Either way, the first sign of a bigger picture shift would be for rates to level-off and spend several weeks holding in a broadly flat trading range.