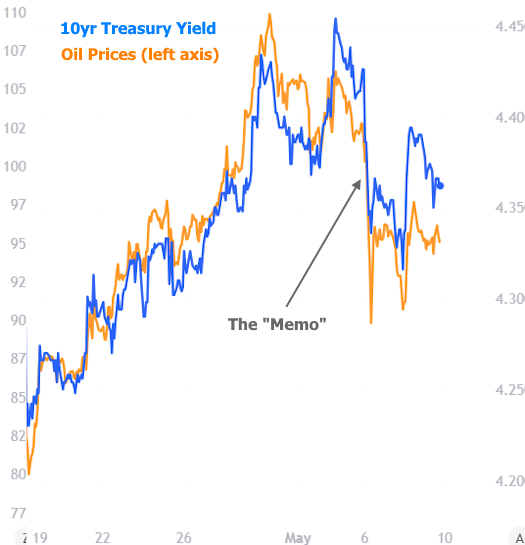

Wednesday ended up being the most interesting day of the week for rate movement thanks to headlines suggesting The U.S. and Iran were close to signing a one page memo to end the war.

Why a memo?

A more formal peace agreement will be a lot longer than one page and will take a lot more time to hash out. If parties can agree, in principle, on the ultimate details, it allows the war to end immediately rather than wait for the formal agreement.

Why do rates like this news?

Rates are based on bonds. Inflation is bad for bonds (i.e. it pushes rates higher). Higher oil prices contribute to higher inflation. And, of course, the war has been responsible for a huge surge in oil prices. Thus, ending the war should result in relatively lower oil prices, inflation, and rates.

We've seen this dynamic play out frequently since the start of the war. It's easiest to see when we use 10yr Treasury yields as a stand-in for mortgage rates because mortgage rates are only updated 1-3 times a day.

How did mortgage rates react?

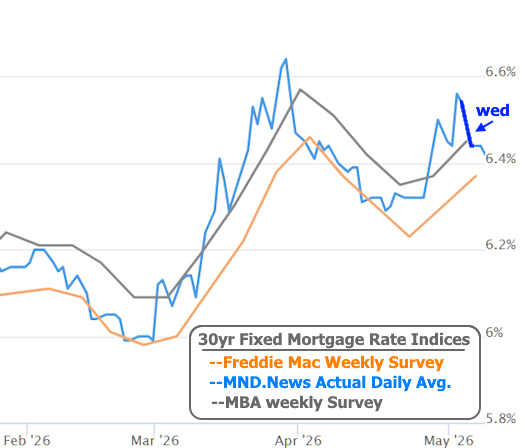

Mortgage rates began the week at the highest levels in more than a month. Wednesday singlehandedly took average daily rates back to last Friday's levels according to MND's daily rate index. Meanwhile, weekly rate surveys (which don't capture movement in a timely way) showed rates moving higher.

What about the rest of the week?

This weekly newsletter would normally have quite a lot to say about Friday's jobs report. The payroll count came in at 115k versus a median forecast of 62k. At almost any other time in history, this would be a surefire recipe for a rapid rate spike to end the week.

But labor market dynamics have been changing in a way that makes the payroll count more of a moving target compared to the unemployment rate (another statistic from the same jobs report), and that came in right in line with expectations at 4.3%.

Labor market dynamics aside, the rate market is simply preoccupied with the war and oil prices. All of the above allowed rates to drift just a hair lower on Friday.

What's next?

The war will continue as the focal point next week, but there will be more economic data. In some ways, it could be more important that the jobs report because two of the reports will provide an update on inflation for the month of April (the Consumer Price Index on Tuesday and the Producer Price Index on Wednesday).