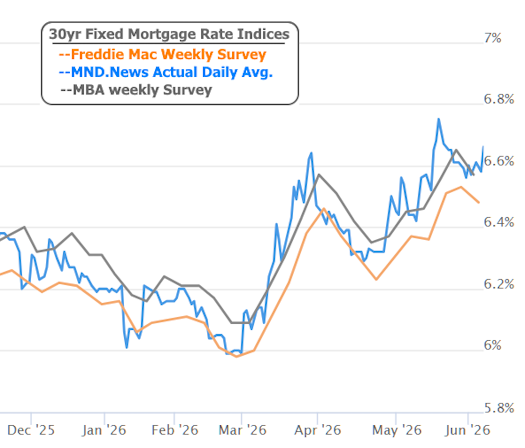

While they're not yet back to the recent long term highs seen on May 19th, mortgage rates surged to 2-week highs on Friday after an exceptionally strong jobs report. This is a bit out of character based on recent norms.

Over the past three months, mortgage rate movement has been driven primarily by developments in the Iran war. It's not that war, itself, is a consideration, but rather the implications for fuel prices and inflation. Bonds care deeply about inflation and interest rates are based directly on bonds.

When inflation isn't raging (or at the risk of raging), rates/bonds spend most of their time thinking about the economy. Lately, the data has been sufficiently even-keeled that it hasn't had enough of an impact to override the war's inflation-related volatility, but Friday's jobs report was an exception.

The jobs report is always the biggest consideration when it comes to monthly economic reports, but like other data, its impact had been limited of late. This particular report was so unequivocally strong that it sent shockwaves throughout the entire market.

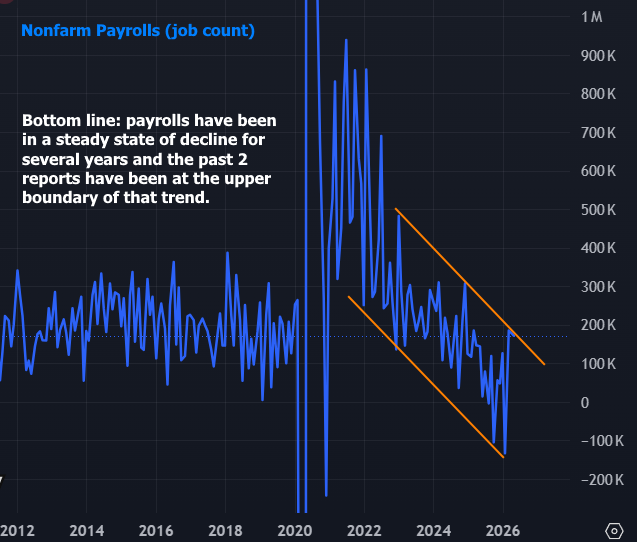

Job growth crushed the forecast of 85k for the month of May by surging to 172k. If that had been an isolated phenomenon, the market might not have cared too much, but the revisions to the past 2 months completely changed the market's understanding of the present labor market.

Back in April, the jobs numbers for March came out at 178k--very high, but at the time, an isolated outlier in a sea of mediocre data. Then in early May, April's job count fell to 115k and the market remained indifferent to the data.

Jobs data is always revised for the trailing 2 months as additional survey responses come in late. In this week's case, that resulted in hefty upward revisions. The 178k from March became 214k and April's 115k became 179k.

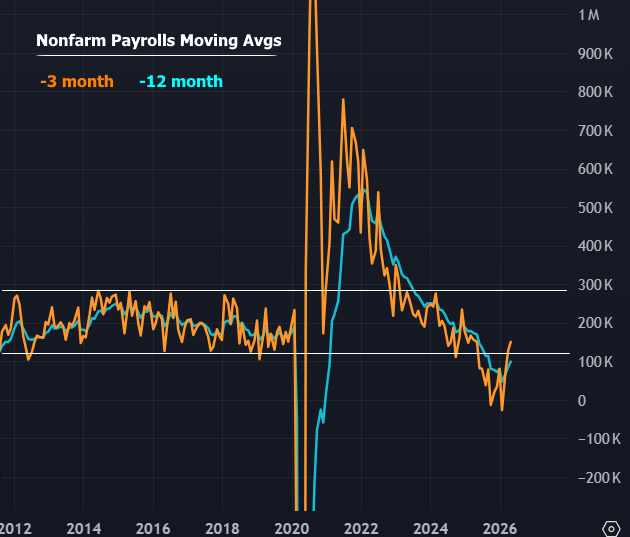

With that, in a single moment, the labor market went from looking like it was in a general downtrend to a firm show of support. Some would even say there's re-acceleration. It's easier to make a case for this when viewing a moving average of the job count in order to smooth out some of the volatility.

Others would say the broader downtrend remains and recent results merely test the upper boundary of that trend.

The choice of description doesn't matter. To the market, it was a compelling argument that the Fed is in no position to consider rate cuts, regardless of the Iran war and, if anything, is far more likely to consider rate hikes later this year, and especially by March of next year, with Fed Funds Futures now indicating 2 rate hikes. Before the Iran war, the expectation was to have seen 2 cuts by then--a total swing of 1.00%.

The broader rate market takes immediate cues from such rapid shifts in Fed rate expectations. Mortgage rates were no exception.

For those seeking solace, in addition to the fact that rates remain under the recent highs from May 19th, it continues to be the case that a confirmed peace deal between the U.S. and Iran would likely facilitate another meaningful drop. In addition, labor market data has indeed been more volatile than normal due, in part, to lower survey response rates--especially evident after last year's government shutdown. Ultimately, this week's reaction to the data will only be indicative of a broader uptrend in rates if additional data sings the same tune or if the Iran war drags on.