Last week's newsletter flagged an uncommonly high level of quarter-end trading volatility as a key contributor to a surprise mid-week rate spike. We got another dose of that drama this week, but things calmed down by the end.

Bond market drama creates rate drama because rates are directly based on bonds. Due to the immense size and complexity of the bond market (and broader financial market), and because trading strategies can vary based on who's doing the trading, there is no satisfying way to measure exactly why things happen the way they do at quarter-end.

What we do know is that a massive amount of money changes hands in a very short time window, with a lot of last-minute settlement taking place right up to the end-of-quarter cut-off. There's also quarter-end trading that begins impacting trading levels several weeks in advance, but it was the "last minute" stuff that hit the bond market this week.

This resulted in Tuesday's rates jumping quickly higher for no apparent reason. Wednesday added a bit of an aftershock as mortgage lenders got caught up with Tuesday's volatility (some lenders don't fully account for all the volatility in a trading day if it happens late enough in the day).

All told, this took the average 30yr fixed rate an eighth of a point higher on the week as of Wednesday. What happened next was a mixed blessing depending on which side you root for. Fans of strong jobs growth got bad news on Thursday morning with June's job count coming in at 57k--well short of the 110k median forecast.

But as is ever the case, bad news for the labor market is generally good news for rates. Bonds improved following the data and mortgage rates managed to recover almost half of the ground lost earlier in the week.

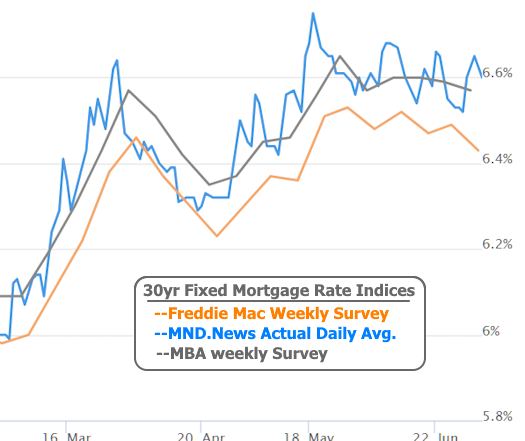

Nonetheless, the week ends with 30yr fixed rates 0.07% higher than last week for the average lender. NOTE: weekly survey-based rate data (i.e. MBA/Freddie Mac) showed lower rates this week because their methodologies have not yet captured Wednesday's rate spike (Freddie technically has, but its impact is diluted because it's averaged with the preceding 4 business days).

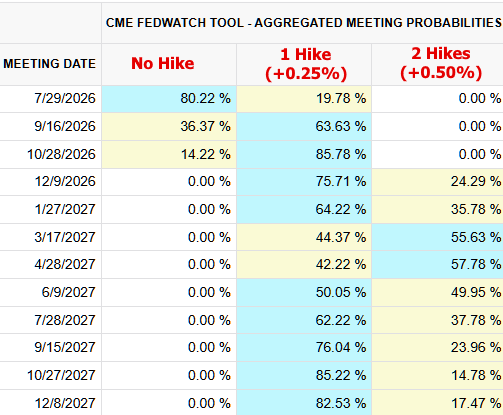

Bottom line: rates are higher this week, but thankfully still not as high as they were in early June or mid-May. Next week brings a smattering of economic data in addition to the minutes of the most recent Fed meeting. The market continues pricing in a higher likelihood of Fed rate hikes by the end of the year.