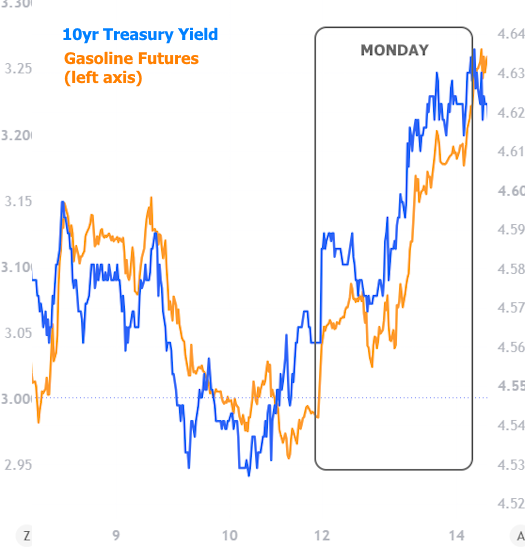

It was an eventful week for mortgage rates and the bond market, but ultimately a decent one. Monday's rates matched the highest levels in nearly a year, but by Friday, we were actually just a hair lower versus last Friday. Here's how we got there.

Following news of more U.S. air strikes in Iran, fuel prices jumped higher on Monday. As has been the case for much of July, higher oil/gas/diesel puts upward pressure on rates via inflation implications (because rates are driven by bonds and bonds hate inflation).

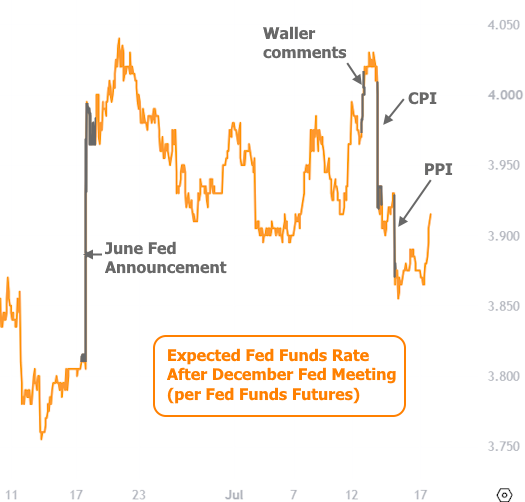

Coincidentally, Tuesday and Wednesday were set to offer two major updates on inflation via the government's Consumer and Producer Price Indices (CPI and PPI). Fed Governor Christopher Waller added to the tension by saying the Fed would need to consider raising rates "in the near term" if those reports came in hot.

Waller's comments represented the first major dose of forward guidance from a Fed official since Warsh took the helm. Warsh has repeatedly expressed his intent to minimize forward guidance from the Fed. As such, the candor and content of Waller's comments had a bigger impact than they otherwise might have if multiple Fed speakers had been making similar comments over the past few weeks. Simply put, it led the market to price in the highest odds of a Fed rate hike since the week of the last Fed announcement in mid June.

Thankfully, the inflation reports pushed back in the other direction, and forcefully! Data's impact on bonds is almost always driven by the gap between the median professional forecast and the actual results. The key metric in Tuesday's Consumer Price Index (CPI) fell farther below that forecast than any other CPI release in more than a year. Other components of the data were similarly below forecasts.

The following day, the Producer Price Index (PPI) put on a similar show with a much bigger drop than expected. Additionally, there was also a substantial downward revision to the previous report. All told, annual PPI ended up an entire 1.0% lower than initially reported last month.

After both of the inflation reports, the market reaction was immediately apparent--especially in terms of Fed rate hike expectations. Traders use Fed Funds Futures to bet directly on the level of the Fed Funds rate at various points in the future. Before Tuesday's data, traders saw the Fed Funds Rate just above 4% (effectively suggesting a 100% chance of a rate hike) by December. After Wednesday's PPI, that had fallen to 3.86% (effectively pricing out most of the risk of a 2026 rate hike).

As we often discuss, when the Fed actually hikes or cuts, it means almost nothing for longer-term rates like mortgages (it's old news by the time it happens). But changes in Fed hike/cut expectations have a big impact. This week was no exception. Longer term bonds like 10yr Treasuries and the bonds that underlie mortgage rates improved sharply--even if not quite as sharply as Fed Funds Futures. This resulted in the average top-tier 30yr fixed rate moving down roughly an eighth of a point between Monday and Friday.

The economic calendar is very light next week and the Fed will be in its blackout period ahead of the late-July announcement. That removes many of the usual scheduled sources of volatility, but war-related headlines remain capable of causing fuel price shocks that spill over into rates. Big moves in stocks could also cause spillover in the bond market in either direction (i.e. a big stock sell-off could help rates whereas a big stock bounce could pull rates a bit higher).