It was a hotly anticipated week, mainly due to the scheduled release of important inflation data on Tuesday, but the rate market almost got more than it bargained for thanks to unexpected headlines the following day.

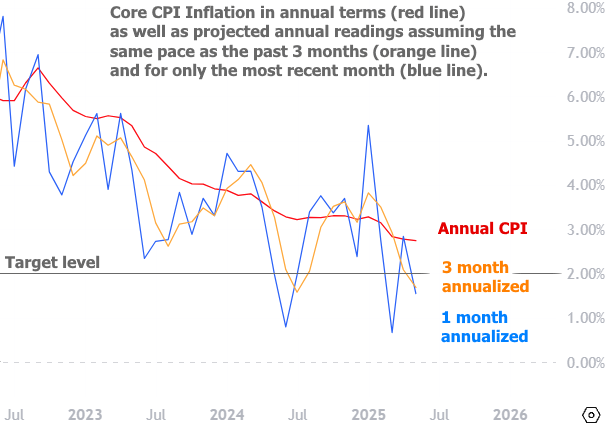

Tuesday’s Consumer Price Index (CPI) provided the first major, national glimpse of inflation in June. It was also the biggest opportunity yet to see whether tariffs were impacting the numbers--a fact that many recent Fed speeches had reiterated. In a nutshell, if tariff impacts were absent, markets would conclude the Fed would be more keen to cut rates sooner. Needless to say, that created plenty of anticipation.

As it happened, CPI came out higher than last time, but lower than expected.

Normally, that would be good news for mortgage rates—and in the first hour of the market's reaction, that’s exactly what we saw. But the celebration didn’t last long. As traders dug into the details, they noticed subtle signs that tariffs were beginning to push up prices in certain areas—even if it wasn’t enough to affect the overall number.

That gave markets a reason to believe the Fed would remain cautious about cutting rates. The result: a sharp reaction in the bond market that pointed toward higher mortgage rates. It wasn’t a massive move, but it kept rates in a higher range relative to the beginning of the month.

Then came Wednesday's "fun with headlines" courtesy of unnamed sources.

After a fairly boring morning with slightly lower rates, reports emerged that Trump had discussed firing Fed Chair Jerome Powell. Markets took the idea seriously. Bonds (which dictate rates) traded at volumes not seen since the April tariff announcements, and longer-term Treasury yields (which correlate strongly with mortgage rates) moved abruptly higher.

That may sound counterintuitive. After all, replacing Powell might seem like a step toward lower rates, right? But we have to remember a few important details:

- The Fed only controls the shortest term rates. The rest of the spectrum can vary quite a bit. The longer the term of a bond, the more it can vary.

- Mortgage rates aren't directly set by the Fed in the first place. They're driven by those longer term bonds.

- Demand for those longer term bonds can suffer (lower demand = higher rates) if investors feel that the Fed might cut rates too much or too soon.

- Unjustified cuts can cause inflation concerns and rates hate inflation.

- Demand could also be impacted by lower investor confidence due to politicization of the Fed's policies.

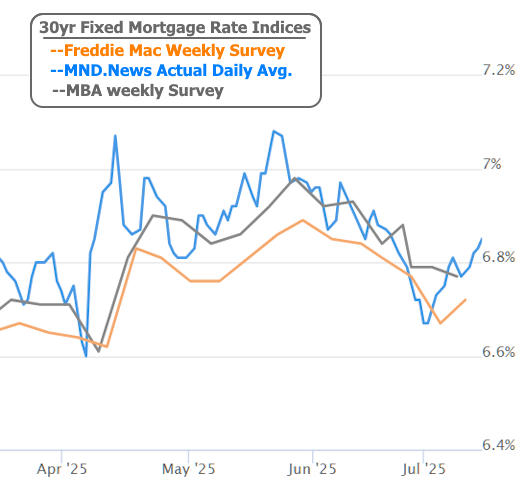

Trump ultimately issued a statement saying that, although he had discussed the idea, he’s not actually considering firing Powell. That helped cool things down a bit. Mortgage rates actually didn't rise too much because mortgage lenders only make adjustments a few times a day (and the news came and went before most had reacted).

Nonetheless, it was a vivid example of a few things we often revisit:

- Unexpected headlines can always make rates move in unpredictable ways.

- Mortgage rates aren't based on the Fed Funds Rate, but they react instantly to changes in Fed Funds Rate EXPECTATIONS, usually by moving the same direction (when the motivation is organic in the economy), but sometimes counterintuitively (when the motivation is external)

The rest of the week felt pretty underwhelming after that. Thursday brought a mixed bag of Retail Sales data. Overall sales were higher, but after adjusting for inflation, they pointed to weakness in discretionary consumer spending. That was modestly rate-friendly, but didn’t do much to change the bigger picture.

"Underwhelming" could be a theme for a few weeks, actually (barring unexpected headlines, of course). We won't get the next round of decisively important data until the first week of August. Now that tariffs are seeping into inflation numbers (albeit modestly), the big jobs report (typically released on the first Friday of the month) is even more important. Low unemployment is the reason the Fed can justify waiting to cut rates. If unemployment begins rising, it would overshadow the type of tariff impacts seen this week. But if it stays steady, rates will struggle to move significantly lower.