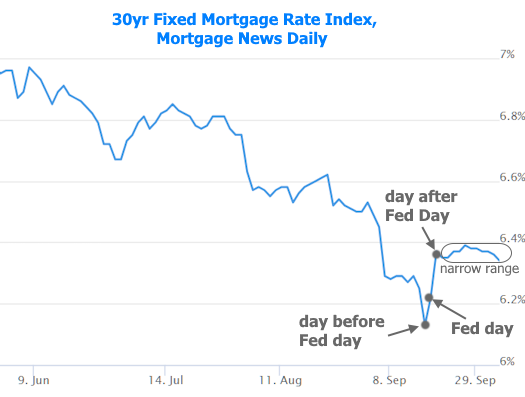

Contrary to mainstream notions regarding the Fed rate cut, mortgage rates moved sharply higher on Fed Day as well as the following day. Since then, they've been in a calm, sideways range, but managed to trickle to the lowest levels in that range by the end of this week.

This is a logical outcome considering this week's bond market movement. 10yr Treasury yields (the most visible part of the bond market that tends to move in the same direction as mortgage rates) moved consistently lower overall with most of the improvement seen on Monday and Wednesday.

Wednesday's gains came courtesy of the ADP Employment report which came in much weaker than expected. ADP's report attempts to predict the job count seen in the official jobs report which is almost always released 2 days later.

In the current case, ADP had the jobs count at negative 32k for the month of September. It also revised last month's 54k to -3k. ADP revisions typically aren't very notable. This one was bigger because it involved an annual re-benchmarking based on the official jobs report from the Bureau of Labor Statistics (BLS).

The BLS jobs report was not released 2 days later, nor will it be released until the government shutdown ends. If it had been as weak as the ADP report, rates almost certainly would have dropped more than they did. As it stands, rates ended up just barely lower than the very narrow post-Fed range.