If we stopped paying attention at noon on Thursday, it was an uneventful week due to an absence of important economic data, a holiday closure, and a lack of volatility in the underlying bond market. After that, things got interesting.

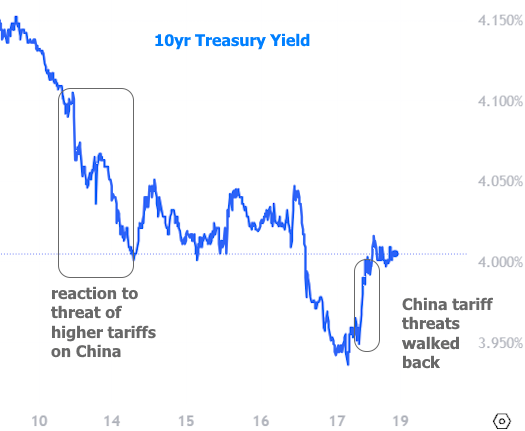

To be fair, things were fairly interesting at the end of the previous week owing to an escalation in trade war tensions with China. With minutes to go on Friday, Trump announced a new 100% tariff that sent stocks and bond yields screaming lower. By the end of this week, yields bounced after Trump walked those comments back, but not before some serious volatility on Thursday.

Warning: the next 2 paragraphs are unavoidably esoteric, but the takeaway is simple.

Things changed precipitously just after noon ET on Thursday. Investors had been bracing for more serious fallout after Zions Bancorp announced it would take a $50 million loss in Q3 due to bad loans. A separate bank, Western Alliance, also announced hefty write-downs tied to similar loans.

The juxtaposition of the news and the involvement of some big-name Wall St firms created significant volatility in short-term interest rates. That volatility was complex due to competing implications for the broader economy (good for rates) and short-term funding markets (bad for rates). When more dire concerns about short-term funding markets didn't materialize, the net effect was a delayed reaction that ultimately helped the entire spectrum of interest rates move lower.

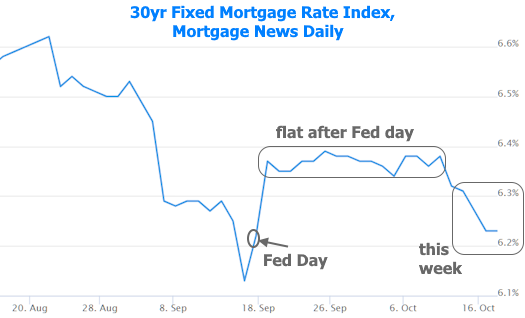

Because bond yields correlate with mortgage rates, it was no surprise to see them moving lower in tandem over the holiday weekend. But at that point, mortgage rates were only beginning to break below the flat, narrow range that's persisted since the week of the Fed rate cut in September. Thursday's bond market volatility added to those gains, bringing the average lender closer to last month's lows.

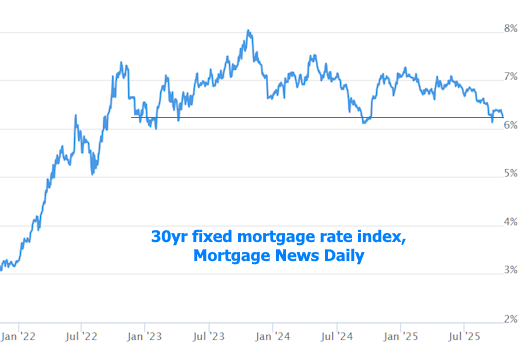

Incidentally, those recent lows are the effective lower bound going all the way back to late 2022.

The incoming week brings the release of the Consumer Price Index (CPI). This will be the first major exception in terms of government economic data releases during the shutdown. While CPI isn't quite as big of an influence as the still-on-hold jobs report, it will nonetheless be one of the most tradeable calendar events for rates in several weeks. As always, there's no way to know if it will help or hurt until the report comes out.