With the announcement that Trump nominated Kevin Warsh to be the new Fed Chair, there's a lot of misinformation and speculation making the rounds regarding the potential impact on mortgage rates. Let's clear it up.

Who is Warsh and why do people think he could be good for rates?

Frankly, it doesn't matter who Warsh is. Trump was only ever going to nominate a Fed Chair who was amenable to additional rate cuts, right? As such, the core question is about whether a rate-friendly Fed Chair will be good for rates.

Sidenote: it's puzzling that people only began talking about this after Warsh's nomination because it was a foregone conclusion that we'd have a rate-friendly Fed Chair nominee many many months ago.

Would mortgage rates benefit from additional Fed rate cuts?

No. A Fed rate cut, in and of itself, does nothing to help longer term rates like mortgages. By the time the Fed cuts, the factors supporting that cut have long since been traded into the bonds that underlie longer term rates. This is why there's typically broad correlation between the Fed Funds Rate and longer term rates despite stark examples of counterintuitive movement by the time the Fed actually cuts.

If you haven't read our primer on the topic, here it is.

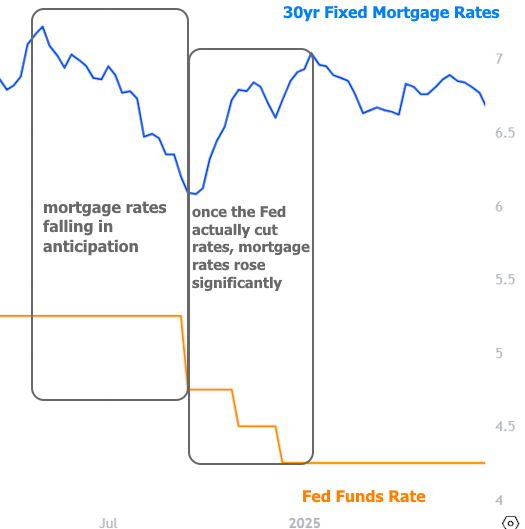

Then why does everyone talk like Fed rate cuts would help mortgage rates?

Because they are wrong. Seriously... Just show them this chart of what happened in late 2024 when mortgage rates hit long-term lows on Tuesday, September 17th--a day before the Fed cut rates for the first time in years. Mortgage rates vaulted appreciably higher over the next several months, even as the Fed continued cutting rates.

But seriously, I hear/think/feel that there will be renewed downward pressure in interest rates across the board once this new Fed Chair is running the show.

There's no viable way you can know this ahead of time. You can only assume (as we all do) that the new Fed Chair will be that much more willing to cut the Fed Funds Rate compared to the last Fed Chair. As discussed in the primer linked above, the Fed Funds Rate is not the same as a mortgage rate.

But let's assume you are right. At that point, you would need to consider efficient market principles. In other words, if your outlook is informed by sources that are available to others, then the market can trade that outlook accordingly. Traders in the bond market would lose a lot of money if they sat on their hands in spite of knowledge that mortgage rates would fall with any degree of certainty in the future.

When such certainties exist, traders trade accordingly and interest rates reflect those changes in real time (or by the end of the business day in the case of mortgage rates). Simply put, if you can know it, so can bond traders, and it is a foregone conclusion they will trade accordingly. Bottom line: any tactical advantage you thought you had based on what you think is going to happen has already been wiped out by the fact that you can't kindly ask traders to wait to act on the same information.

I'm tired of arguing with you. Did anything interesting happen this week?

Thursday was the most interesting day when it comes to mortgage rates and market movement. There were three employment-related economic reports that painted a more downbeat picture for the labor market. Bonds/rates love bad news, so it ended up being the best day of the week for mortgage rates.

To be sure, part of the reaction was fueled by positioning ahead of next Wednesday's jobs report (the biggest and most important labor market report of any given month). If that jobs report confirms the contraction, rates could continue lower--possibly flirting with the long-term lows seen in January. On the other hand, if the jobs report is merely in line with expectations, that could erase part of the improvement seen this week. And if the data is markedly stronger, rates would almost certainly be moving up to the highest levels since December.