The bond market drives changes in interest rates. Among bond traders, it's no secret that the Bureau of Labor Statistics' (BLS) jobs report is the most consequential monthly economic data. But this time around, the reaction defied expectations.

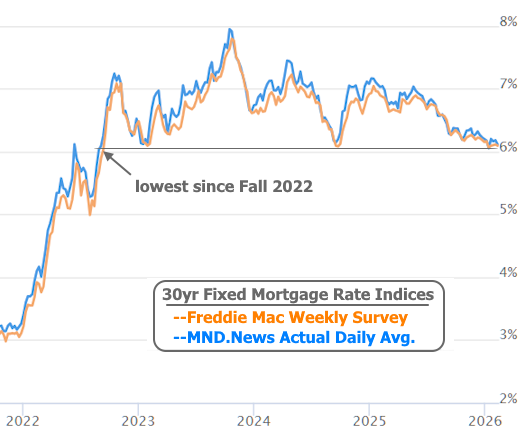

Specifically, if you were to tell market participants the results ahead of time (i.e. 130k jobs created versus a forecast of 70k, and a 4.3% unemployment rate versus a 4.4% forecast), 9 out of 10 would have bet on interest rates ending the week noticeably higher than last week. As it stands, Treasury yields hit the lowest levels in months, and Mortgage Rates fell in line with the lowest levels since August 2022.

It wasn't that the jobs report had any sort of paradoxical impact. Indeed, Treasury yields and rates spiked in the immediate wake of the news. But in addition to being at the lowest levels in weeks just ahead of the data, rates spent the next 2 days more than erasing the damage from Wednesday's jobs data. The following chart shows this phenomenon in 10yr Treasury yields, which tend to move much like mortgage rates.

If we zoom that chart out and change the symbol to a daily candlestick (a single mark that shows the day's trading range and open/close levels), we can see just how much more volatile AND rate-friendly things have been since last Thursday.

What accounts for this? Please note: all of the analysis that follows is merely a collection of some of the most plausible explanations. Many seasoned bond market pros are on record saying they're stumped by this week's resilience.

We know that last Thursday introduced 3 labor market metrics that were quite weak. That economically negative message was compounded this Tuesday by a Retail Sales reading that was much lower than expected.

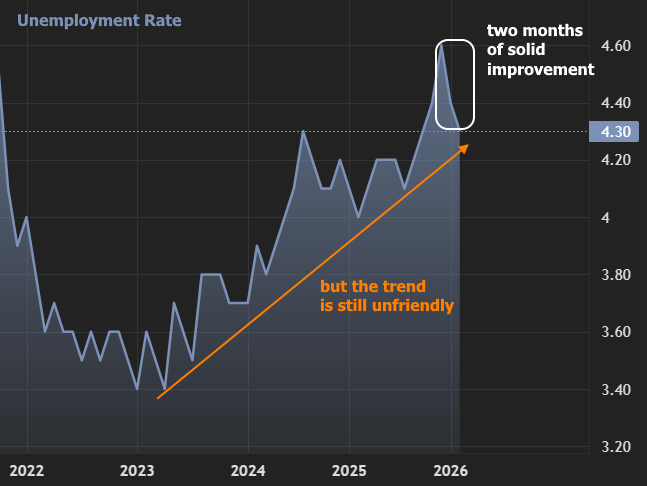

Looking beyond the strong jobs report headlines, some caveats can be constructed. For instance, even though unemployment was lower than expected, the trend remains unfriendly (which is good for rates).

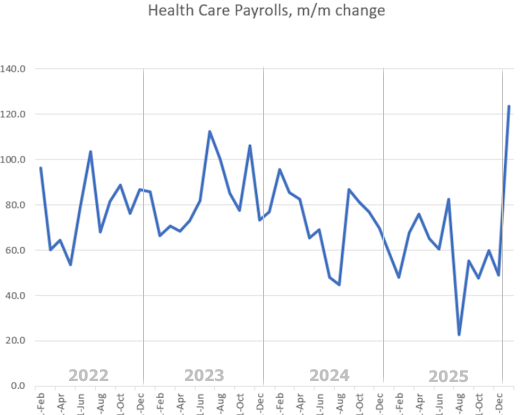

In addition, although the payroll count was much higher than expected, the health care sector may have added jobs at a pace that is unlikely to be seen in subsequent months. Case in point, it was the largest monthly change in healthcare payrolls in years, and more than double any of the recent readings.

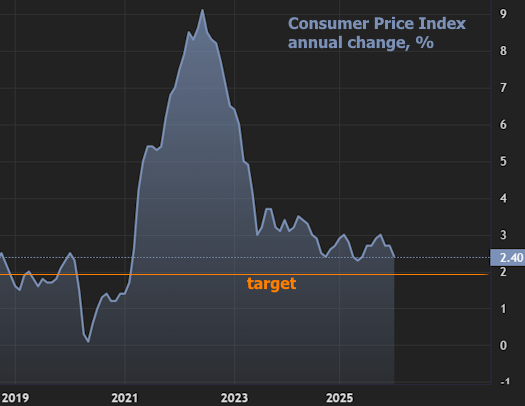

Additional economic data helped rates on Friday with the Consumer Price Index (CPI) coming in a bit lower than expected. CPI is the first major monthly inflation data, and inflation is an important consideration for interest rates. Headline CPI continues to tick toward its 2% target and was 0.2% lower than the market expected for this report.

All that having been said, the analytical challenge is to explain lower rate momentum that was transpiring without any help from econ data. Thursday was the most notable day of the week in that regard. It also happened to be a day of heavy selling in stocks and commodities.

It's a mistake to assume that weakness in stocks will always correspond with lower interest rates, but it's generally more common to see rates/yields move lower on days with very large stock market declines (the major exception is when markets are moving due to changes in Fed rate cut expectations--not the case on Thursday). In the bigger picture, recent bond market resilience could be as simple as investors sensing that the current phase of stock market expansion is at risk of taking one of its period breaks. The effect of such a recent "break" can be seen on 10yr yields in the following chart.

Granted, early 2025's volatility was compounded by tariff announcements, but past examples are nonetheless similar. Last but not least, we can always consider some additional volatility potential surrounding 3-day holiday weekends.

When markets return next Tuesday, the economic data slate is not quite as robust, but we will get several housing-related reports throughout the week. Friday brings our first look at GDP for Q4-2025 as well as a more thorough reading of inflation for December via the Personal Consumption Expenditures (PCE) data.