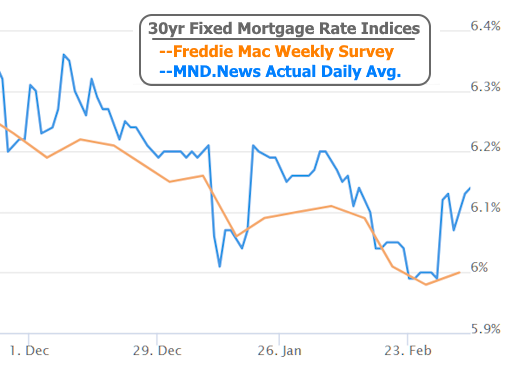

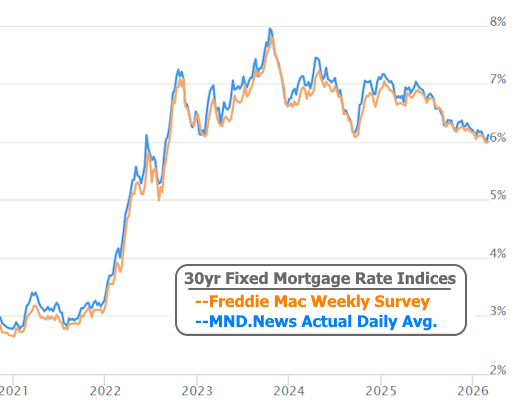

Last week, it seemed interest rates could do no wrong. Mortgage rates started at multi-year lows on Feb 23rd and proceeded to have a record-setting week (lowest weekly volatility for any week that began with multi-year lows).

This week has been entirely different. A chart of 10yr Treasury yields allows us to see minute to minute changes in long-term rate momentum.

In terms of mortgage rates, this made for a jump back into the early February range.

For the sake of perspective, it should be noted that this isn't a massive jump in the grand scheme of things.

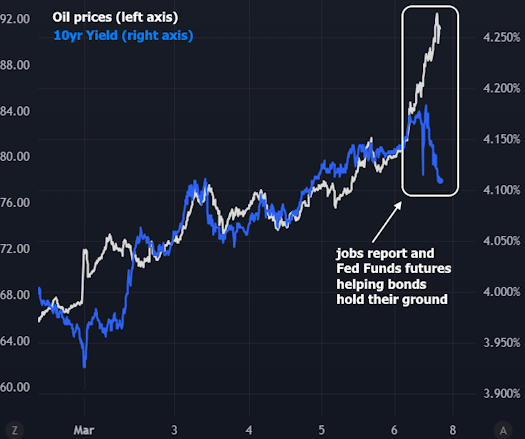

Reasons for the volatility are somewhat debatable, but there are a few that everyone is talking about. The biggest news of the first 4 days of the week was undoubtedly the massive spike in oil prices stemming from the armed conflict in Iran.

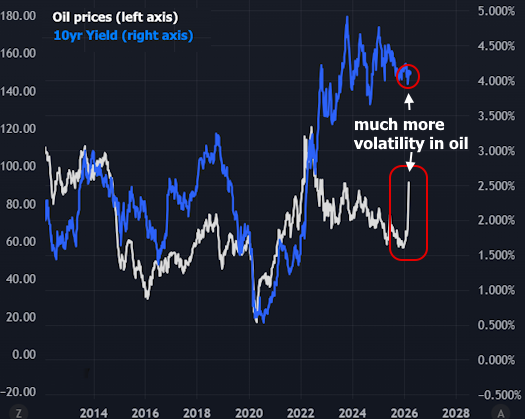

As a key input for shipping costs, oil prices have logical implications for inflation. In turn, inflation is a key consideration for interest rates. Notably, it takes a fairly dramatic shift in oil price momentum to register a response in the bond market. As seen in a longer-term chart, bonds haven't seen a fraction of the volatility in oil.

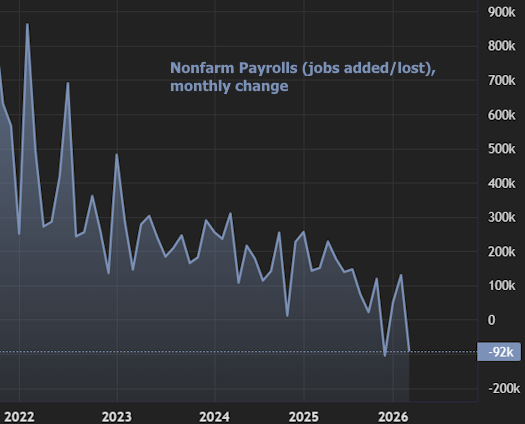

If we zoom in to the present week, the correlation is blatantly obvious. It only broke down after an exceptionally weak jobs report on Friday.

Nonfarm Payrolls (a count of jobs added/lost each month and the headline metric of the jobs report) came in at -92k versus a median forecast of +59k.

That's an incredibly big miss, and obviously a low reading, but the market has recently broken from decades of precedent to place even more importance on another metric from the same report: the unemployment rate. Here too, the results were not bullish for the labor market, but the bad news arrived in more measured steps with the unemployment rate ticking up to 4.4% from 4.3% last month.

It's worth noting that this is historically low territory, and it's really only the trend that is potentially troubling (not the outright level).

Other data from earlier in the week suggests that rates will continue keeping an eye on economic growth and inflation implications of oil prices. Monday's manufacturing index from ISM showed the highest "prices paid" component since 2022.

Wednesday's service sector index (also from ISM) suggested economic resilience, also coming in at multi-year highs.

The collision between that economic resilience and higher price pressures has been playing out in bits and pieces over the past 2 years, but it's thrust into the spotlight by the surge in oil prices. In the coming weeks, the rate market will continue taking cues from any inflationary impulses in commodities prices while we wait for big ticket econ data to either offset or exacerbate the price pressure.