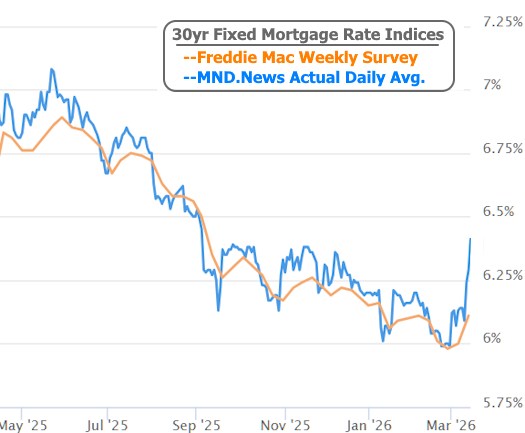

February ended with 30yr fixed rates at the lowest level in more than 3 years. There's been a grueling march higher since then with average rates ending the week at 7-month highs.

While the first few days of March were open to some debate about the reasons for the rate spike, there's now only one elephant in the room, and it's a war elephant.

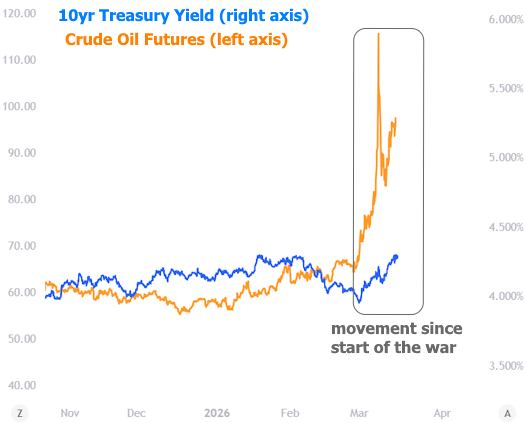

Wars have various effects on financial markets depending on geography, U.S. involvement, and the impact on the global economy and inflation. When wars cause obvious disruptions of critical supply chain components, rates see upward pressure due to inflation implications.

In simpler terms, oil is a key input in the cost of transporting almost any physical good almost anywhere in the world. If war in Iran is pushing oil prices abruptly higher, the bond market is forced to anticipate higher inflation in the future. The result: higher interest rates today.

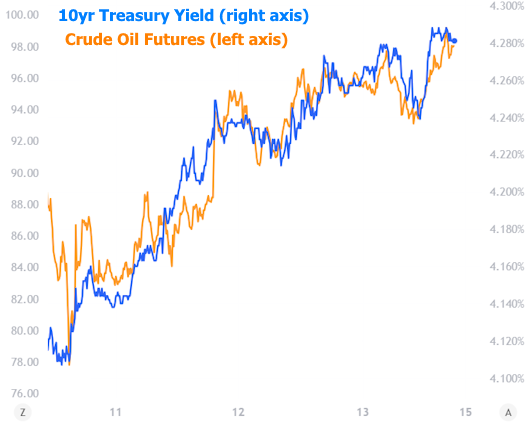

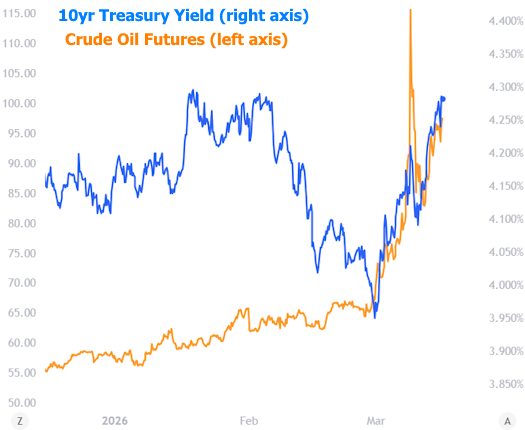

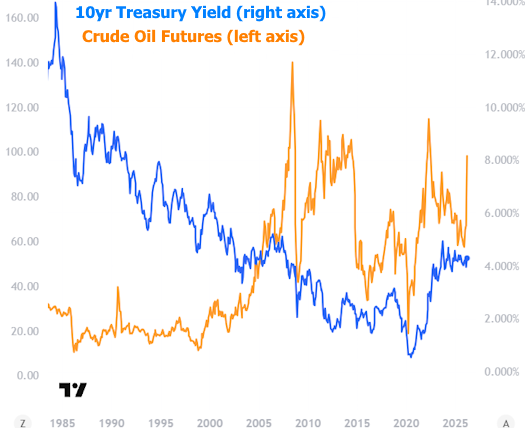

At this point, we'd like to take a quick moment to clarify and comment on the relationship between oil and rates. Many people mistakenly believe they're joined at the hip due to episodes like this and charts like the one seen above. Oil and rates share common motivations (like "the economy") so they often correlate, but they also share opposing motivations (like currency valuation). Last but not least, always consider the amount of time presented in any given chart, and be curious what that chart might look like with a longer time frame or different y-axis scaling. Three examples follow:

There are a few other forces that may be contributing to rising rates at the moment, but they'll be easier to measure once the oil price rout is reversed. The uncertain timeline for such a reversal is yet another problem for financial markets. On several occasions this week, markets swooned in response to newswires that implied an open-ended timeline.

Unfortunately for interest rates, returning to February's lows won't be a simple matter of the war being over. Oil prices (and other inputs, like natural gas and fertilizer) have taken a big enough hit and supply chains have been sufficiently delayed/disrupted that the market will assume a certain amount of latent momentum in consumer prices. Bond buyers will be cautious about buying too aggressively (bond buying = lower rates) until inflation data gives the "all clear," and that could take several months.

None of the above means rates can't turn a corner and move lower--simply that it might not be as soon or as robust a reversal as many rate watchers may be expecting.

Can/will the Federal Reserve save us?

Simply put: no. Not under Powell and not under Warsh. While the Fed will meet next week to announce its rate decision for March, there's no chance they'll be cutting in light of current inflation risks. There will be no reason for the Fed to consider its next rate cut until/unless inflation inputs drop significantly or the economy deteriorates abruptly.

Even then, the Fed would only be cutting short-term rates. It's the rest of the bond market that determines longer-term rates like those for mortgages. We have several recent examples of longer-term rates moving higher following Fed rate cuts.

Bottom line: the best hope for rates is for a big drop in energy prices and, to whatever extent you feel OK hoping for such things, a weaker economy.