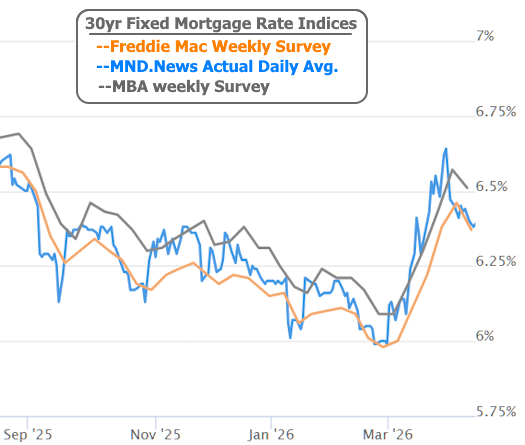

Whereas the entire month of March was "up, up, and away" for interest rates, April has been far calmer by comparison. The average lender ended the week in slightly lower territory and there was less volatility to boot. Refreshingly, the lower volatility means that weekly surveys were aligned with daily rates in showing the modest drop (unlike last week).

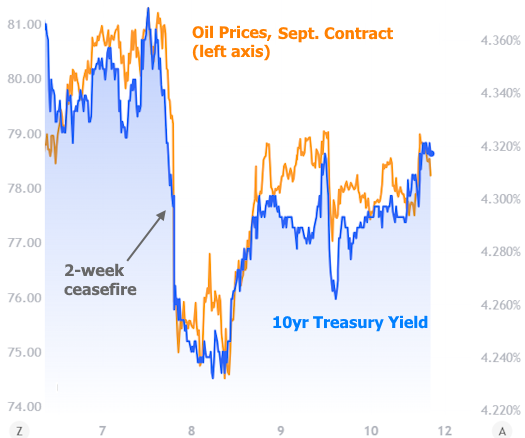

That said, there's no question that the Iran war remains the most compelling source of market motivation. Inflation is the key reason--specifically inflation implied by oil prices. Tuesday's ceasefire news had the biggest impact. It caused a quick drop in oil prices. Interest rates (represented by 10yr Treasury yields in the charts below) followed, but everything bounced back a bit as the ceasefire was increasingly tested in various ways in the second half of the week.

As the mortgage rate chart suggested above, there's still a long way to go before erasing the war-related impacts.

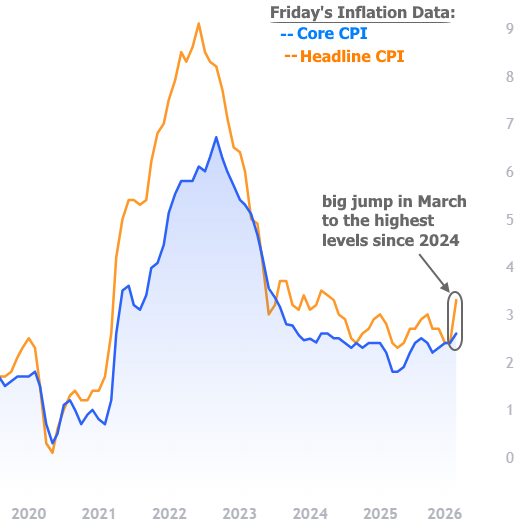

Unlike last week, this week offered better evidence of oil prices impacting official inflation data. The Consumer Price Index (CPI) came out on Friday at the highest year-over-year level since 2024.

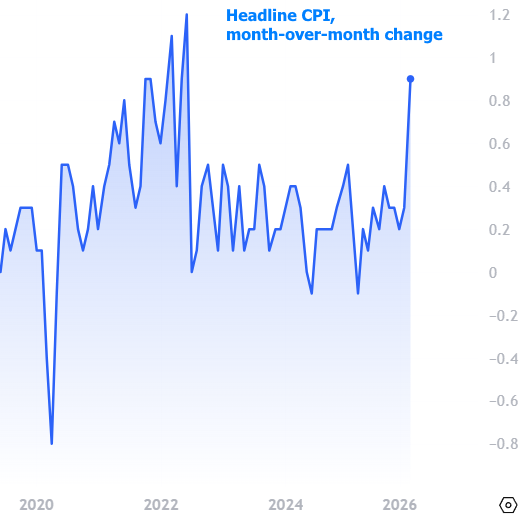

It may not look like much on the chart above, but the bond market has been hoping to see monthly inflation growing at a pace just below 0.2%. This latest report was more than 4 times faster, and twice as fast as any month from the past several years.

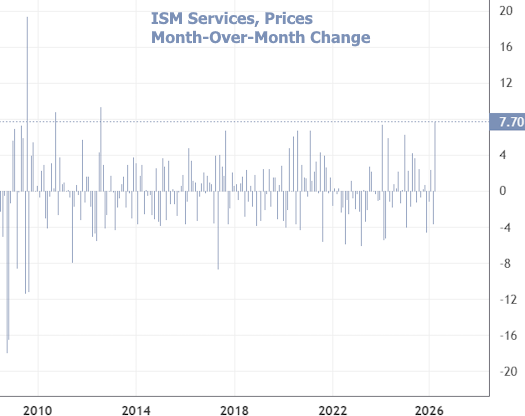

The inflation is showing up in other data as well. This week's most notable example (apart from CPI) was the price index component of the ISM Services data which hit the highest level since 2022.

Here too, the month-over-month change was a problem. ISM hasn't recorded a bigger change since 2012.

The upcoming week is much lighter in terms of scheduled economic data, leaving the market free to focus solely on energy price fluctuations driven by geopolitical developments.