Mortgage rates moved lower almost every day this week with most of the help coming from war-related headlines and a last-minute boost from the jobs report.

Rates are driven by bonds and the bond market dynamic is surprisingly simple these days. Oil price volatility is a constant source of inspiration with rates generally moving in the same direction as oil. Additional considerations include the usual suspects like big-ticket economic reports and any notable updates from the Federal Reserve.

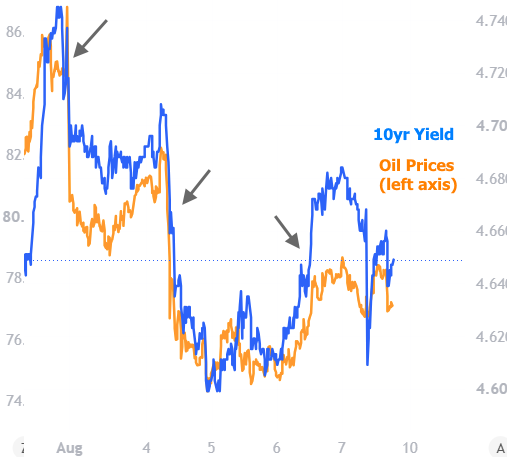

This week saw several positive developments in Iran, either related to the pace of fighting or the prospects for reopening the Strait of Hormuz. Oil prices responded accordingly and bond yields (aka "rates") generally followed.

The chart below shows 10yr Treasury yields and oil futures this week with the notable movement highlighted. The additional rise in 10yr yields on Thursday came courtesy of a large corporate bond announcement (this increases supply in the bond market which, in turn, lowers prices and increases yields/rates).

The big drop in bond yields seen on Friday came after the release of the latest monthly jobs report which showed much lower than expected job creation. The job count (officially "nonfarm payrolls") came in at -23k versus expectations of +80k. Traditionally, that would result in a massive drop in rates. These days, however, markets are more and more interested in the unemployment rate, which actually moved 0.1% lower from last month.

How can the economy lose jobs but have a lower unemployment rate? The latter is a math equation based on the total number of people who consider themselves "in the job market." If they respond to a survey saying they have a job, they count as employed. Meanwhile, the official job count comes from business surveys. It can show a decline in the number of jobs without impacting unemployment if fewer people say they're in the market for a job.

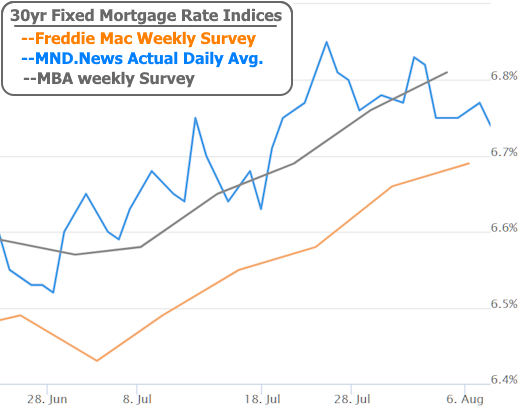

All that having been said, rates still improved from Thursday to Friday, ultimately ending the week at the lowest levels since July 20th. Weekly, survey-based rate indices have yet to catch up to the drop in daily rates measured by Mortgage News Daily.