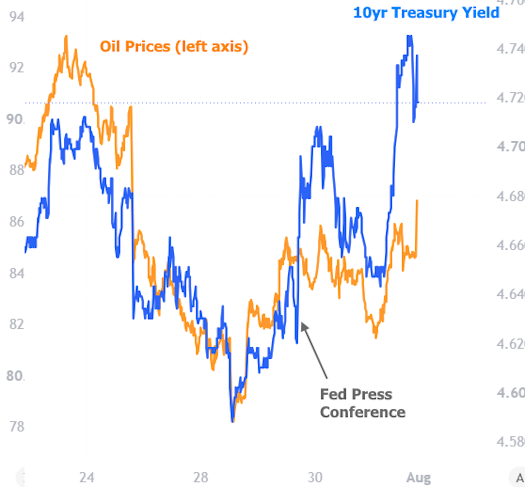

If there's one thing to know about this week's rate movement it's that it left us almost exactly where we were last Friday. How we got there felt a bit more dramatic at times.

The week began on a hopeful note following Sunday's news of a pause in the fighting in Iran. Oil prices moved lower in response and rates followed. Those good vibes lasted all the way through the first half of the week. It wasn't until Wednesday afternoon's Fed announcement that we saw a meaningful reversal. To make matters worse, it wasn't really a logical reversal at first glance.

Futures markets suggested a 1 in 3 chance that the Fed would hike rates this week. They did not hike. You might view that as good news for rates. Markets did too... initially.

Problems arose shortly into Fed Chair Warsh's press conference. Different Fed watchers have slightly different ideas as to what mattered most, but most agree that the key concern involved mentioning alternative measurements of inflation data beyond the traditional Personal Consumption Expenditures (PCE) data set.

Some took this as a suggestion that he may favor data that paints a better inflation picture in order to keep rates lower than they otherwise might be. The counterpoint is that he could simply be referencing a goal to expand the data set that the Fed considers without abandoning a commitment to 2% PCE inflation. This is arguably relevant at times when PCE is trending in a certain direction and more granular data could help suggest that trend continues.

Beyond that, some felt that the market gave the committee the green light to hike rates at this meeting and demonstrate a firm commitment to the inflation target, and by not hiking rates, some bias toward lower rates was revealed. At this point in Warsh's tenure, it is too early to make such claims, but that's not to say they didn't inform the way some traders reacted.

Lastly, on a purely qualitative note, some traders reported feeling that Warsh was talking tough on inflation without doing enough to reassure markets that he knew what conditions would warrant a rate hike. Their conclusion: if Warsh won't comment on the Fed's current reaction function (a separate matter from forward guidance) then markets will take matters into their own hands by selling bonds in the longer end of the yield curve (e.g. 10yr and 30yr Treasuries and, to a lesser extent, mortgage rates).

This newsletter offers no judgment on the views shared above. The goal is to relate market chatter that followed the press conference. Objectively, all we know is that the long end of the yield curve did indeed swoon during the press conference despite initially reacting fairly well to the 2pm Fed announcement itself. For whatever else it's worth, the swoon ended when the press conference ended.

The week's only other key event was not so much an isolated event as the general trading dynamic that played out on Friday. It involved additional Treasury selling (which pushes rates higher) in response to currency intervention in Japanese Yen. When Japan seeks to bolster the Yen's value, one strategy can involve selling sovereign debt of other countries. Excess selling pushes rates higher all else equal.

Esoteric currency considerations aside, Friday also saw oil prices move up moderately in addition to firmer inflation data in the form of the Employment Cost Index. Last but not least, it was also a month-end Friday in July--something that can create random, elevated volatility simply due to the way financial markets wrap up their accounting for the end of the month (with the July/Friday part simply connoting lighter trader participation which traditionally adds potential volatility).

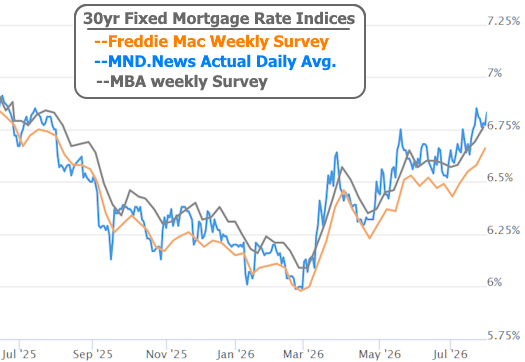

All told, mortgage rates moved up to the second highest level in more than a year, but again, only modestly higher versus last Friday.

In the coming week, oil price volatility remains relevant. We'll also get the latest jobs report on Friday which is always one of the two most closely watched economic reports as far as rates are concerned.