Mortgage rates hit 5 month lows last week but quickly jumped to the highest levels in more than a month this week. While last week's strong jobs report certainly served as a catalyst, there's more to the story.

Fortunately, the story is fairly simple. It began in October when rates hit decades-long highs and finally began to make progress back toward lower levels. Inflation had been a pivotal component of the surge and inflation reports were starting to moderate in November and December. Simply put, a rate recovery made good sense.

In fact, lower inflation was desperately anticipated by financial markets. Interest rates, especially, had been on the defensive, waiting for a sign that the worst was over. Q4, 2022 arguably provided that sign, but there were serious questions to be answered about what would come next for rates.

The market began answering those questions in January. Mortgage rates and popular benchmarks like the 10yr Treasury yield had fallen an entire percentage point, but then paused to wait for the green light to drop some more.

Rates were right to be hesitant. By falling as much as they had, they were already playing a dangerous game of chicken with the Federal Reserve. The Fed controls and sets the shortest-term interest rates in an effort to control inflation. The Fed Funds Rate doesn't directly dictate mortgage rates, but changes in the Fed's rate outlook definitely impact mortgage rates. Conversely, a big enough drop in mortgage rates can carry implications for inflation (the thing the Fed is trying to fight by raising short-term rates).

Here's where that game of chicken comes in. The market had been betting that the Fed would be forced to cut short-term rates by the end of 2023 even though Fed members had repeatedly said rates wouldn't top out for a few more months at minimum and then remain at the ceiling for a year or two. The market thought the Fed was bluffing or wrong. Either way, those defiant expectations helped mortgage rates hit 5 month lows last week.

Then the jobs report happened (last Friday). It also happened 2 days after the Fed's latest policy announcement. Markets began to panic. What would the Fed have done if it knew the jobs report would be so strong? Panic was amplified by the fact that Fed Chair Powell was scheduled for an informal Q&A the following Tuesday (February 7th) at the Economics Club of D.C. (a venue that would surely generate relevant questions).

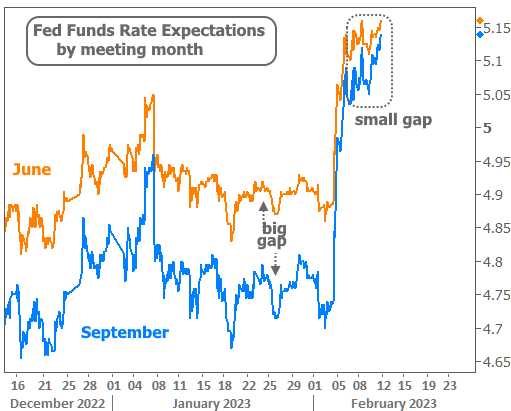

Even before Powell took the stage, the market was already rethinking its game of chicken. Whereas Septembers Fed Funds Rate had consistently been expected to be lower than June's, traders were quickly beginning to believe it would be unchanged. The following chart shows those expectations over time, both for the June and September Fed meetings. Note the gap that had existed up until this week.

By the time Powell spoke on Tuesday, the market was already admitting defeat. All Powell had to do was say that last week's jobs report is exactly the sort of thing the Fed has in mind when it says inflation may be more persistent than the market thinks and that rates may need to stay higher, longer than the market things.

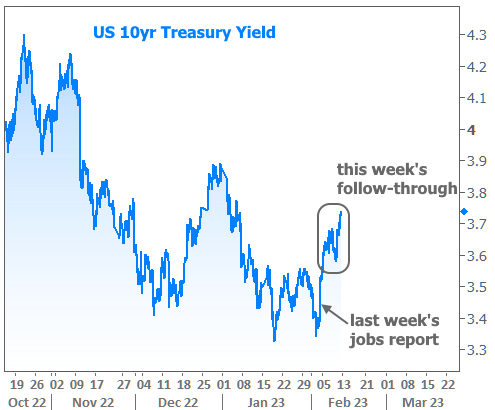

As the week progressed, additional Fed speakers joined in with similar messages. The net effect has been a quick move off the recent lows for longer-term rates. They're now up to the highest levels in more than a month.

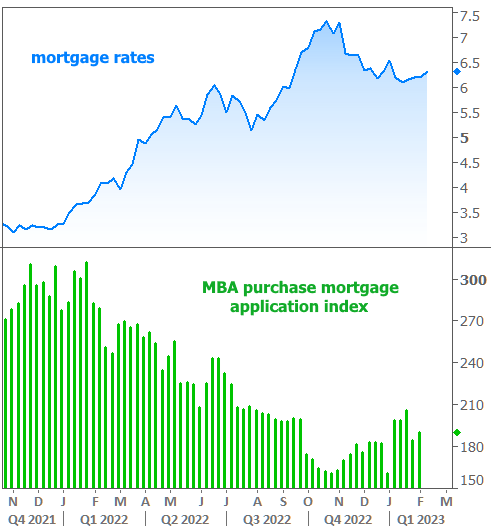

Momentum in mortgage rates has been similar with the average lender up roughly half a percentage point since last Thursday. This has implications for purchase mortgage demand based on the typical correlation seen in the following chart. Specifically, the drop in rates helped bring prospective buyers off the sidelines. It wouldn't be a surprise to see this week's rate spike take a toll on the momentum.

While the current week has been one of correction and reversal, it's important to know that it doesn't carry an implication for the next move. This week was about the market catching up to the Fed's messaging and giving up a bit of the exuberance it may have felt after identifying what we all hope will prove to be a very long-term top in rates last fall.

Even then, this week's move required economic data to serve as a catalyst. Heading into the coming week, we can expect more of the same. Tuesday's Consumer Price Index (CPI) is the only economic report that could be argued to be more important than last week's jobs report. If inflation falls more than expected, rates should be able to recover back into the recent range. But if inflation comes in much hotter than expected, we could be in for another panicked move higher.

How high? It would take more than one CPI report to get mortgage rates back to last year's long-term highs, but if other economic data was similarly strong, it could only take a week or two in the most dire scenarios.

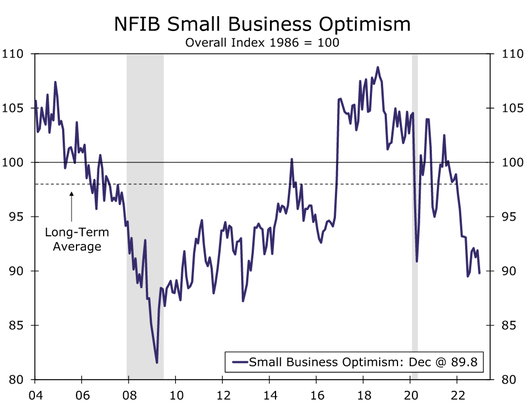

If the jobs report was so strong, should we worry about other data singing a similar tune? Yes and no. We should be sensitive to the possibility that the economic data measured by government agencies will be different than our individual perceptions of the economy. So many of the answers depend on where you look. For instance, consider another report set to come out on Tuesday: Small Business Optimism.