Markets have settled into a cycle that favors the jobs report as the only critical economic data as far as rates are concerned. This week's inflation data had a chance to claim/preserve a role as a strong supporting actor, but instead, it basically stood aside and left focus on the labor market and the Fed's interpretation of recent labor market weakness.

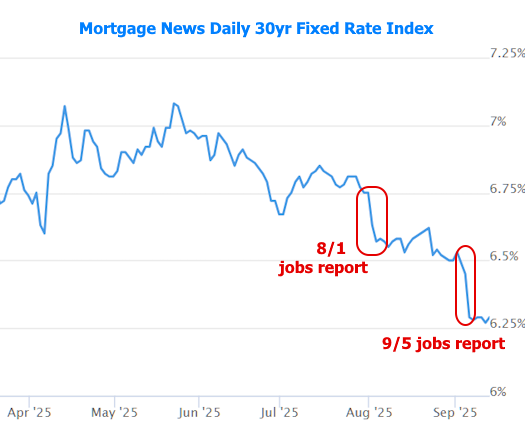

A majority of the notion of "recent labor market weakness" is attributable to the jobs reports from August 1st and September 5th. Taken together, they suggest the labor market is potentially shifting gears in a negative way. Outside of jobs report days, bonds (which dictate rates) have been broadly sideways from one report to the next. September 5th was a bit of an exception as the other labor-related data on September 4th helped fuel an anticipatory "lead-off" that made for a 2-day drop in rates when combined with the weak jobs report on the 5th.

The following chart of 10yr Treasury yields (the universal benchmark for longer-term rates like mortgages) shows this dynamic. The yield after the 8/1 jobs report ended up in almost exactly the same spot by the time the 9/5 jobs report rolled around. Same story with yields seen this week in the wake of the 9/5 jobs report.

There's good reason for this. The Fed has been clear in saying that it is more focused on recent labor market weakness as opposed to still-elevated inflation when it comes to the decision to cut rates. If inflation was getting equal consideration, the market wouldn't be so certain that the Fed will be cutting in September.

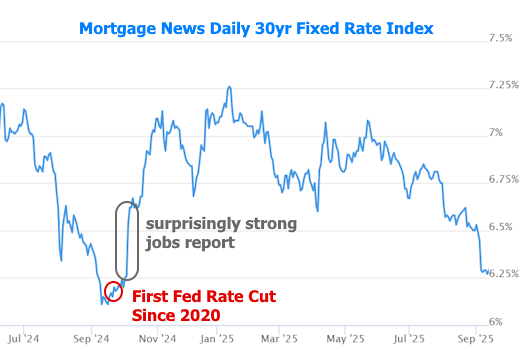

The chart also provides an important reminder that day-to-day interest rates move well in advance of actual Fed rate cuts. In other words, if the market is betting on a rate cut with near 100% certainty, that rate cut has already had its impact on mortgage rates. Thus, next week's rate cut has absolutely NO SIGNIFICANCE for mortgage rates. They've already fallen in response to the same news that's influenced rate cut expectations.

Last year serves as a sobering and important reminder about what CAN happen after a Fed rate cut. Many rate watchers were surprised to see mortgage rates rise significantly starting in October. That life lesson has led to some concern about a repeat performance this time around, but it's critical to remember that the October 2024 rate spike happened because the October jobs report was much stronger than expected.

To be fair, jobs reports aren't the only game in town when it comes to rate movement--merely the most important one. Certain Fed days can be fairly important as well, even when the Fed does exactly what's expected in terms of cutting rates.

The distinction lies with the "dots"--a reference to the dot plot released 4 times a year showing each Fed member's outlook for the Fed Funds Rate in the future. The dots basically let the market know how accurate the market's expectations are for additional Fed rate cuts based on the current trajectory of the data.

At present, the market sees a better-than 75% chance the Fed cuts 0.25% at the two remaining Fed meetings in 2025 (i.e. 3 cuts total in 2025). Next Wednesday's dots will let the market know if the Fed agrees. If the dots show more Fed members in the "2 cut" camp, rates could move quickly higher, but not at the same extreme pace seen in late 2024. For that, the next jobs report in early October would also need to be surprisingly strong.

Bottom line, next Wednesday's dot plot can create some legitimate short term volatility, but the next risk of serious movement is the early October jobs report.