It's that time again, maybe. By this time next week, we will either be several days into another government shutdown or in the throes of volatility following the big jobs report, but it's probably one or the other.

Officially known as The Employment Situation, the monthly jobs report is published by the Bureau of Labor Statistics (BLS), part of the Federal government's Department of Labor. If the government shuts down, so will BLS and that means Friday's jobs report would be delayed.

That's important to mortgage rates because the jobs report is the most consequential piece of monthly economic data. It's especially consequential these days as the labor market is taking the reins from inflation as the primary driver of interest rates.

Even when inflation is in focus, the jobs report is still almost always more capable of causing rate volatility. A delay would mean markets are flying relatively blind and forced to rely on other non-government data like the ADP employment report scheduled for Wednesday.

In the past, there have been instances of the jobs report remaining on schedule despite a shutdown, but that's not as likely to happen this time. At the very least, we should know by Wednesday morning at 12:01am ET.

As for the present week, it was fairly forgettable. There were multiple Fed speeches, but none of the comments rattled the rate market, for better or worse. Thursday morning's strong economic data put only modest upward pressure on rates and Friday's inflation numbers were right in line with forecasts.

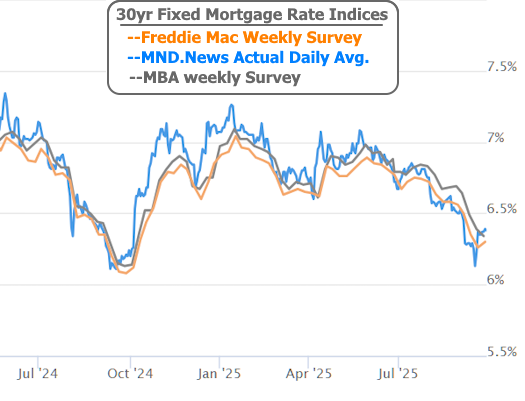

Average 30yr fixed rates held a narrow range very close to last Friday's latest levels.

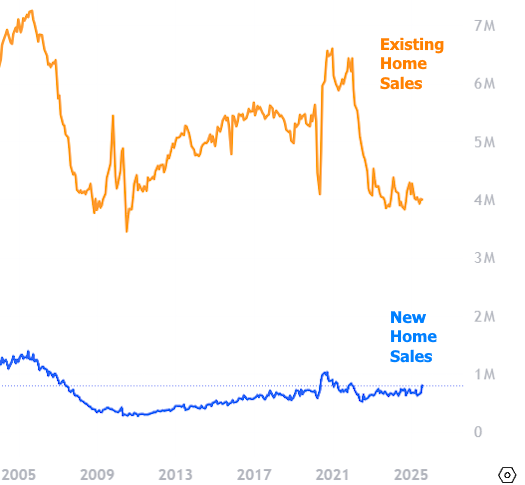

New home sales surged, but in addition to being a volatile data series, new homes don't account for nearly as many sales as existing homes, which continued languishing near long-term lows according to a separate report a day later.

Mortgage refi applications hit another new long-term high, but just barely, and mostly thanks to a tailwind from last week's initially low rates.