This week's potential volatility was supposed to be all about the big jobs report, but an unexpected headline completely stole the show.

On Thursday afternoon, Trump announced he would be directing his representatives to buy $200bln in mortgage-backed securities (MBS). These are the bonds that directly impact mortgage rates and such a level of buying would easily push rates lower.

The initial news prompted immediate questions and some incredulity. But no matter what one's personal opinions may be regarding bold announcements from the President, this one is absolutely serious and the market has already confirmed that.

How do we know?

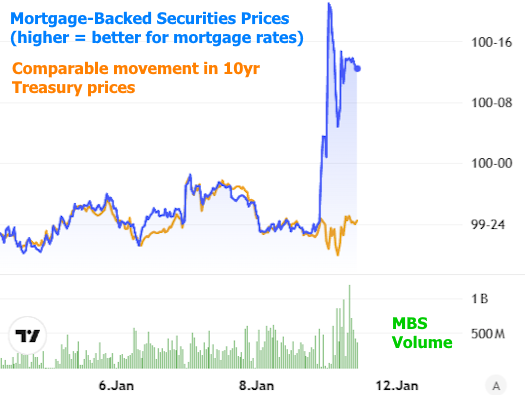

The easiest and most conclusive way to know is to avoid any deep thinking and simply know that the MBS market reacted immediately and forcefully. In other words, traders have already done the mental heavy lifting for you. They wouldn't have been moving billions of dollars of MBS at a time of day typically reserved for wrapping things up and heading home.

In other words, the chart of MBS price/volume doesn't lie. This particular chart also includes the relative movement in Treasuries to emphasize the MBS-specific nature of the move:

Those who want to dig a bit deeper can do just a little bit of math. In his announcement, Trump offered the dollar amount of "$200bln." Incidentally, as of the most recent monthly filings, the GSEs (Fannie and Freddie, the only entities to which Trump could have been referring) have $202.9bln of room on their balance sheets before hitting their current regulatory cap. In other words, $200bln is a carefully chosen number and not some random, off-the-cuff remark.

Perhaps more importantly, Bill Pulte, the director of the FHFA (which oversees Fannie and Freddie), has already confirmed this is the game plan.

Does the president have the authority to do this?

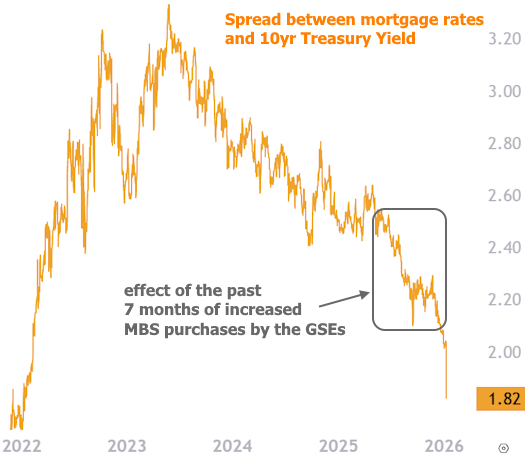

In a word, yes. Under the existing regulatory and conservatorship authority, FHFA can direct the GSEs to buy MBS up to the caps set forth in the PSPAs (the legal documents that govern the conservatorship). In fact, this has already been happening over the past 7 months as GSEs ramped up MBS holdings significantly (roughly $50bln).

Do the GSEs have the money for this? Where would it come from?

Recent filings show the GSEs have nearly $200bln in cash equivalents (actual cash + short-term liquid securities). The money does not come from Treasury or the Fed, etc. In addition, the GSEs are the largest non-sovereign issuer of corporate debt, and they can borrow at rates that would allow them to cash flow new MBS purchases. So the only real limitation is the aforementioned regulatory cap of $202.9bln.

How big a deal is $200bln?

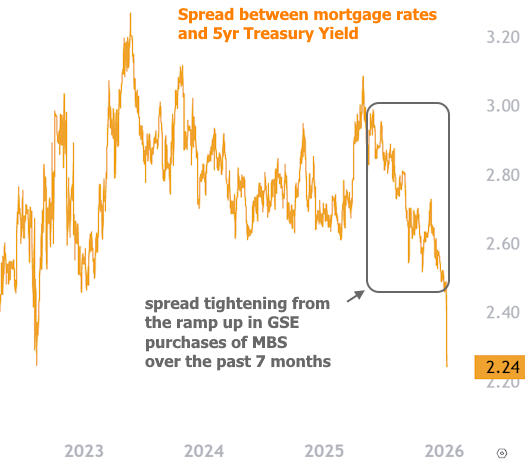

This depends on a few factors, but the reaction in the MBS market is enough to tell you that it matters. Also consider that we can assess the impact of that $50bln of additional purchases over the past 7 months and see what it's done to spreads between mortgage rates and Treasuries.

Conventional wisdom will have most people comparing mortgage rates to 10yr Treasuries, but that's not the right way to assess spreads these days. 5yr Treasuries are currently a better benchmark and will provide a more realistic idea of what that $50bln in MBS buying did for spreads. Granted, there are some other factors at work that can account for the tightening of mortgage rates to 5yr yields, but during the time that MBS purchases were ramping up, that spread tightened by about half a percent (50bps).

There are diminishing returns to additional MBS purchases as this spread continues to compress. If the last $50bln accounted for about 0.30% of spread tightening (0.50% actual - 0.20% likely due to other factors), we won't simply multiply that by 4 and assume another 1.2% drop. But it will be a meaningful impact. In fact, today's rate drop alone was just over 0.20%.

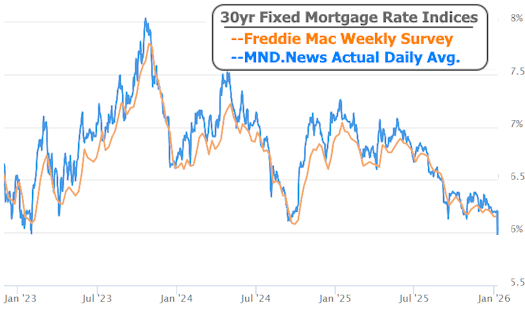

This took the average top tier 30yr fixed rate to the lowest level since February 2, 2023, matching the lowest level in more than 3 years.

Ultimately, the impact over time will depend on the details of how the purchases are conducted. We know the MBS market is definitely already reacting, but that reaction will continue to be volatile and unpredictable as traders rush to price in the unknown impacts of unknown implementation details.

What's the bottom line for now?

This is not Fed-style QE. It's not an ongoing commitment to steadily buy MBS until further notice. That said, it's definitely something and it definitely suggests rates will be left in a better position than before. Exactly how good remains to be seen. Expect volatility.