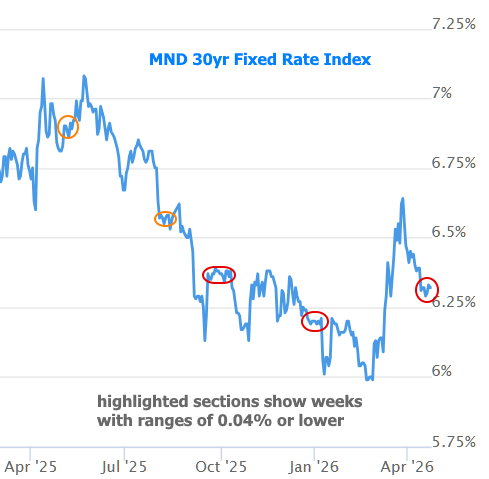

If there were a movie about mortgage rates, this week would be the part where they say "it's quiet... almost TOO quiet." Case in point: MND's daily mortgage rate index has held inside a range of 0.04% since last Tuesday.

This kind of thing happens several times per year. The previous two instances gave way to noticeably sharper movement, but there are older examples that resolved uneventfully.

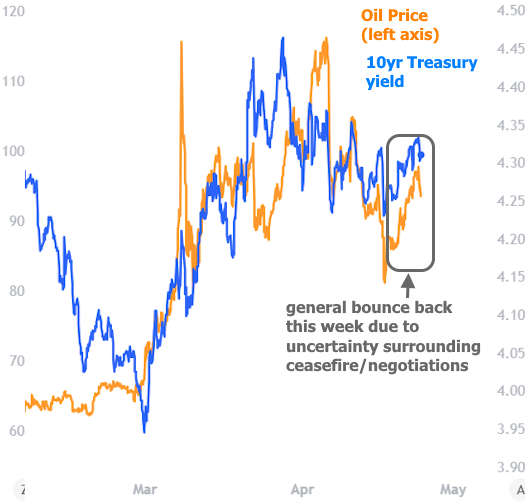

The present indecision reflects the fact that the broader market is waiting for the next big development in the war. Oil prices and bond yields have generally moved higher as the war escalated and lower as prospects for peace improved. They bounced a bit higher this week due to uncertainty surrounding the state of the ceasefire and peace negotiations.

Economic data was very light this week with Tuesday's Retail Sales being the only big ticket report. Even then, the market preferred to trade war headlines and corporate earnings, with the latter helping stocks hit another all-time high.

Next week's economic calendar is slightly more robust, but the market will likely continue to focus on the war-related headlines for primary cues. In addition to the data, there will be a Fed rate announcement on Wednesday, but the market has long since concluded that there is a zero percent chance of a cut or hike.

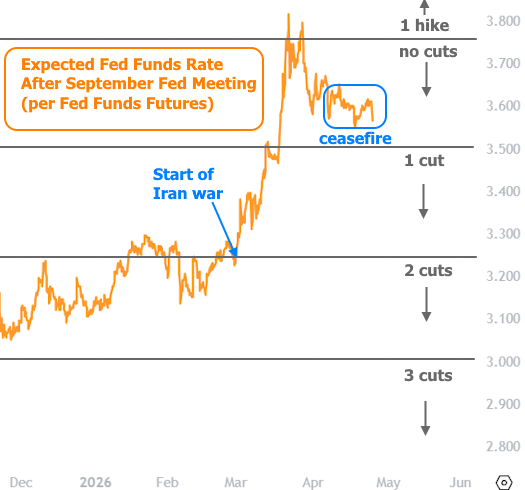

How about later in the year? With the DOJ dropping its case against Fed Chair Powell, some people expect a better trajectory for rates later this year under the presumed new Fed Chair Kevin Warsh. But the traders who bet on those outcomes disagree. There's been very little change in Fed rate expectations over the past several weeks. In short, before the war, the market thought we'd see at least 2 rate cuts in 2026. Now it sees zero. This could change in the future, but it would depend on inflation and economic data.