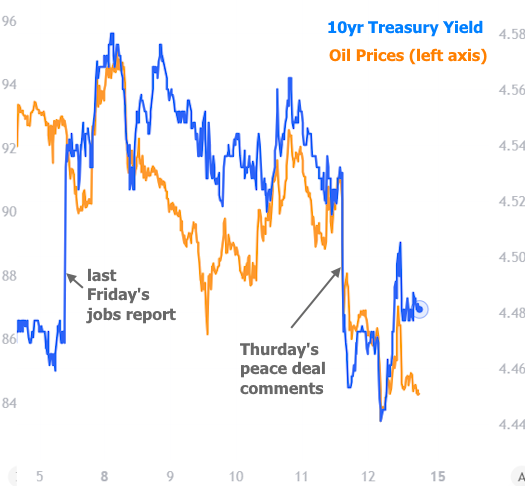

Since late March, markets have had repeated opportunities to play deal or no deal when it comes to ending the Iran war. Sometimes we won. Sometimes we lost. This week's installment was touch and go, but ultimately a winner.

A quick recap of the underlying nuts and bolts:

- The Iran war caused oil prices to spike

- Higher oil implies higher inflation

- Higher inflation begets higher rates

There are ancillary considerations, but the bullet points above account for a majority of the volatility.

Rates began the week higher as fighting continued over the weekend in Iran, but the tone began to shift almost immediately with Israel agreeing to halt attacks in Lebanon. Bonds broke from oil prices later that day (i.e. yields/rates moved higher despite oil prices moving lower), presumably due to a rotation back into the stocks and defensiveness ahead of this week's cycle of Treasury auctions.

The deal/no deal correlations were again in focus on Wednesday as Trump said the U.S. would be attacking Iran "very hard." But the following day, Trump not only cancelled further attacks, but also made the most forceful/convincing announcement of a peace deal so far.

Even though markets take this game with a grain of salt, there was broad willingness to react this time. Bond yields and oil prices dropped sharply. Stocks surged. All that remained was to see whether Iran's response would be "no deal."

Throughout this process, it's been common for one side to refute claims made by the other. While some news outlets released snippets that arguably tried to push back on peace deal prospects, that pushback was markedly softer than previous examples. By Friday morning, we had Iran's foreign minister confirming that the two sides had never been closer to signing a memo that would effectively end the war and begin a more formal peace negotiation.

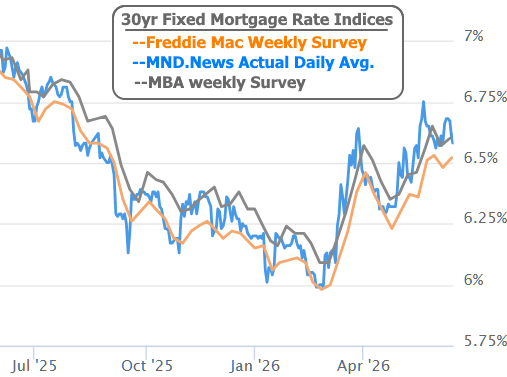

With that, bonds managed to end the week very close to their best levels. Because mortgage rates are based on bonds, 30yr fixed rates hit their lowest level in more than a week. The average lender is only 0.02% above the lowest level in 4 weeks seen on May 29th. The only catch is that the 4-week range consists of the highest rates of the past 10 months.

Heading into next week, we can expect more volatility for better or worse depending on what's in the briefcase. If a peace deal is actually signed, rates would likely drop even more. If hostilities re-flare, we'll continue flirting with long-term highs.

Wednesday brings the next Fed announcement where markets expect effectively no chance of a hike or a cut. Fed day could still cause volatility depending on comments from new Fed Chair Kevin Warsh.