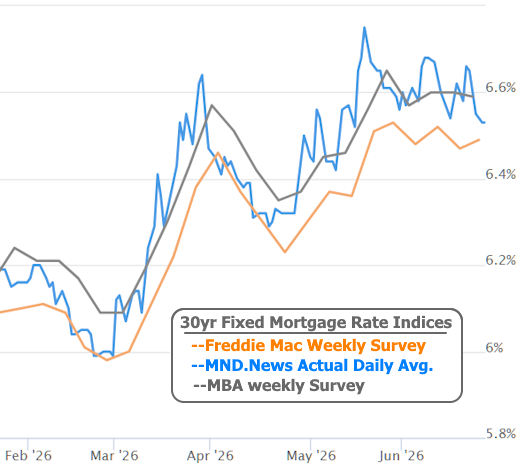

We've had our fair share of big news events causing big reactions in markets over the past few months, but this week offered a welcome reminder that not every improvement in mortgage rates requires a dramatic headline. After moving back toward recent highs early in the week, rates recovered sharply on Wednesday and then managed to hold those gains through Friday, ending at the lowest levels since mid-May.

Some of the improvement was helped by lower oil prices and tame inflation data, but the biggest motivation came from quarter-end trading. Large institutional investors periodically adjust the balance between stocks and bonds in their portfolios. Because stocks have significantly outperformed bonds in recent months, many investors have been buying bonds to restore those targets. Higher demand for bonds translates into lower interest rates.

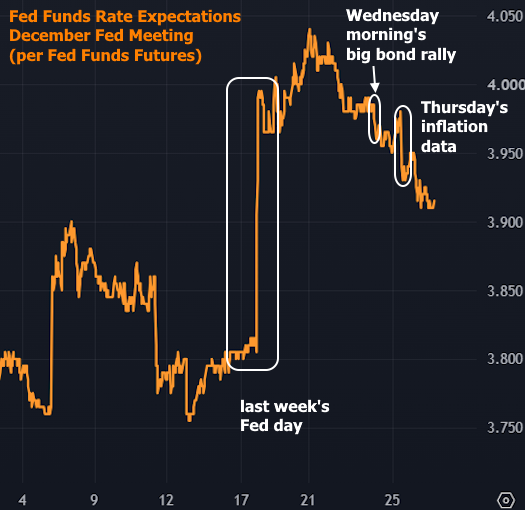

Unlike recent weeks, there wasn't a single dominant news story driving the market. Monday's weakness lacked a convincing explanation, Tuesday was one of the quietest trading days in months, and the strongest gains arrived Wednesday as quarter-end rebalancing demand became more apparent. Thursday was the only potential exception as bonds definitely seemed to benefit from an as-expected reading on a key inflation report, but most of the early improvement faded by the afternoon before giving way to an even more sideways day on Friday.

There's no official way to measure the timing and scale of quarter-end rebalancing. Instead it must be inferred from context. In this case, there's little else that could explain the huge swing in bonds on Wednesday morning. There were no major headlines coming out at the time, and there was no correlated movement in oil prices or stocks (oil was moving lower that morning, but was almost done with its move before bonds started rallying).

Perhaps even more telling was the fact that Fed Funds Futures weren't really moving at all at the time. If there had been something in the news or economic calendar fueling the bond buying, we would typically see it show up here as well.

Regardless of motivations, the results were good for mortgage rates, which spent both Thursday and Friday at their lowest level in more than a month according to MND's daily rate index.

While that's certainly welcome news, it comes with a familiar caveat. There are a few more days left for quarter-end trading to potentially exaggerate market movement in either direction. Still, the bulk of that volatility has likely already been seen.

From there, investor attention quickly shifts back to economic data, which arrives in force next week. Due to the Independence Day holiday, the monthly jobs report will be released next Thursday instead of Friday. It is routinely the most important economic report of the month and has the potential to determine whether this week's improvement is extended or reversed.