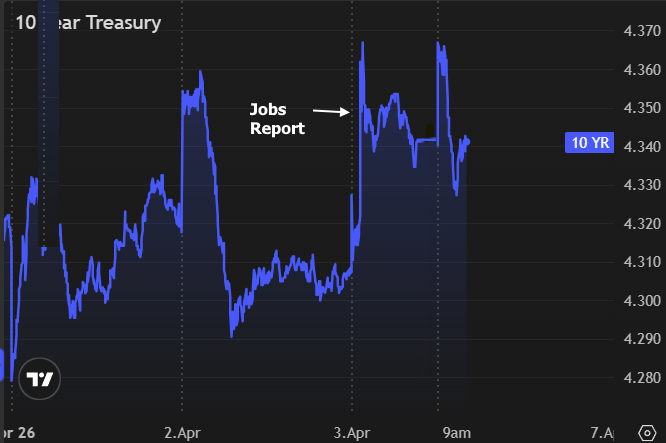

Much of the international trading community remains on holiday today, making for lower volume and liquidity in the US. Bonds have managed to mostly shrug off Friday's stronger jobs report--a fact that we'd attribute mainly to the focus on the unemployment rate over the balmy payroll count. Additionally, war-related developments remain near the top of the heap of relevant market movers until their impacts translate more forcefully to economic data. On that note, we'll get ISM Services data this morning and CPI on Friday--both for the month of March. The weekend offered no meaningful changes in the status of the war other than the notion of a 45 day ceasefire being floated, but not yet approved by either side.